Planemo Intern @PlanemoIntern

@PlanemoTrading algorithmic trading platform for perpetual futures. alpha live on extended, grvt & lighter. https://t.co/zIv1UPznE3 planemotrading.xyz Joined October 2025-

Tweets1K

-

Followers184

-

Following970

-

Likes1K

We launched yesterday on Nado. Just queried builder stats via their official API. Happy to report that we have been the #1 builder over the past 24 hours. Wen official builder stats dashboard @nadoHQ?

gNado! We are live on @nadoHQ. Today we are launching our entire suite of trading algorithms on Nado. This also marks the first time we are making our statistical arbitrage system publicly available across exchanges. This has been a long time in the making, all details in the

gNado! We are live on @nadoHQ. Today we are launching our entire suite of trading algorithms on Nado. This also marks the first time we are making our statistical arbitrage system publicly available across exchanges. This has been a long time in the making, all details in the thread below.👇

We at @PlanemoTrading were among the first 15 users to implement priority fees on @HyperliquidX for internal testing and are a top10 wallet by fees spent so far. From our own tests across 1,000+ transactions, we can see that this update serves effectively as a speedbump for IOC orders on HIP3. Our latency increased by roughly the 8x45ms that is outlined in the docs as maximum possible speed increase. It would be interesting to analyze the current user base of priority fees to find out what strategies are being run that justify implementation. The docs mention the reasoning behind priority fees is to prevent the escalation of an arms race of ultra-fast market makers. We are not ultra-fast nor a market maker. We so far don't see the value of paying 8bps extra just to get the speed we got "for free" a week ago. Our strategy does not necessarily benefit from being faster than other takers, but it certainly hurts performance if we are slower while order cancel/refresh stays the same as pre-update. So looks like some strategies could end up as collateral damage here as an unintended (?) side effect.

Priority fees update. Live on mainnet for 4 days now. Here's what the data shows. Last 24h: Total priority gas burned: 50.41 HYPE Fills with priority: 267,323 Annualized burn (linear): 18.40K HYPE Avg priority gas: 0.000189 HYPE Max single priority gas: 0.318423 HYPE

Last 40 or so days of one of our stat arb users.

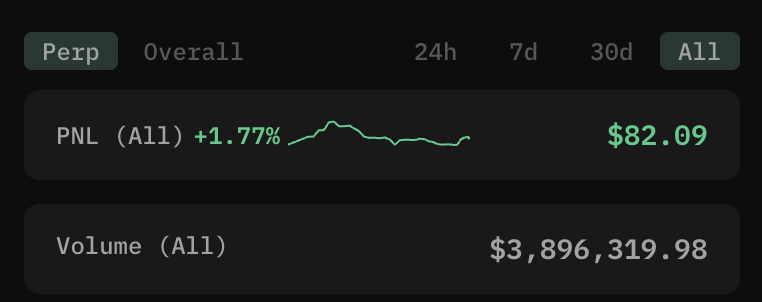

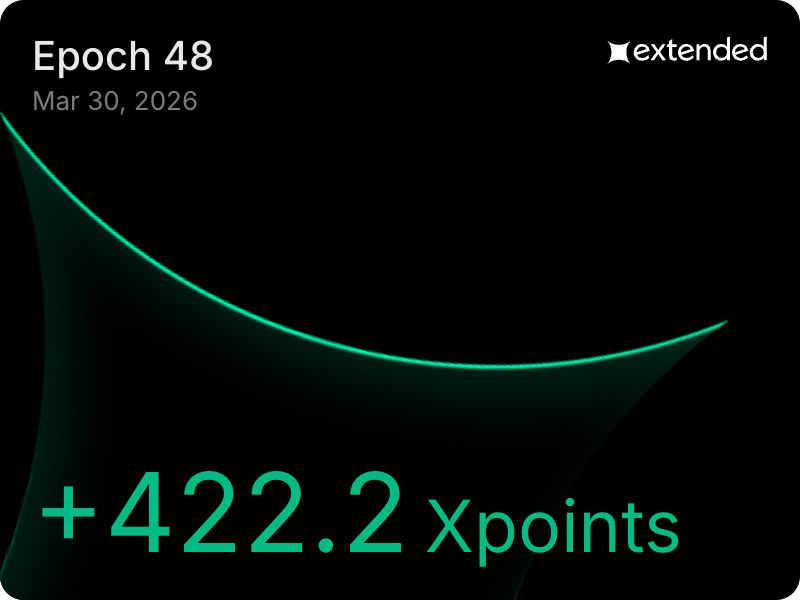

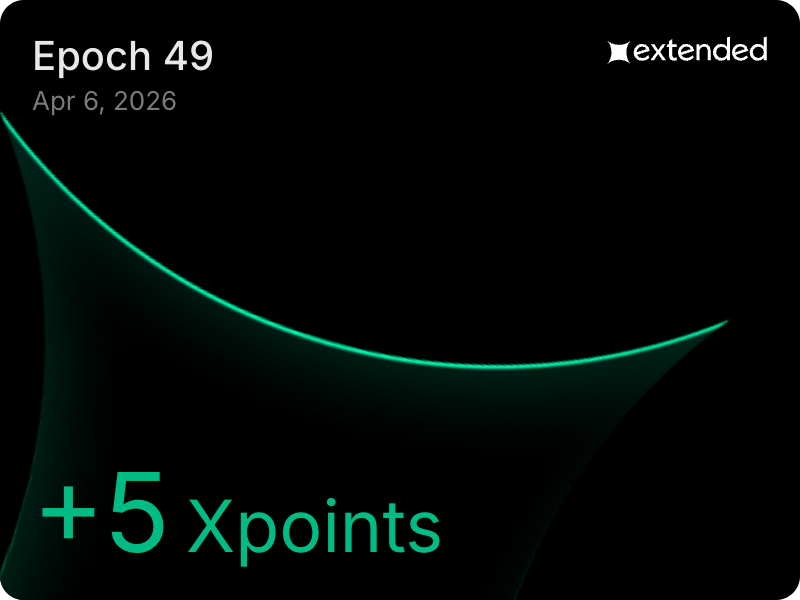

Fun experiment on @extendedapp with interesting results: We let out Surge Pro algo run for 1 week (epoch 48) in combination with having another single open position all week. Stats were $2M in taker (aka more points) volume, with $20k in constant open interest. Costs were $300. Then last week (epoch 49), we deactivated Surge Pro and just kept the open position as is. Stats were just the $20k constant open interest. Costs 0. You can see the results in the screenshots attached, but the amount of distributed points differ by a factor of 80! 422 points vs 5 points. It's been all the rage on Twitter the last few weeks to proclaim that open interest, holding time and whatnot is the number 1 factor for points, but the numbers tell a different story. As long as Extended launches above $150M FDV, it's hard to imagine a scenario in which you lose money with a cost per point basis significantly below $1. A few users have recently done the math and have re-started using our Surge algos for farming Extended. That's also why we are consistently ranked #1 there in terms of volume and fees generated for Extended (more points). Give it a try: extended.planemotrading.xyz

just try it yourself hip3.planemotrading.xyz

Toxic flow is one of the main killers of stat arb profitability. If you want to learn about toxic flow, here's a long post about the basics and how we're building defenses against it. (Implementation will be a quarter-long effort from our engineering team and the first version will likely go online at the end of this month.) When you run a delta-neutral stat arb strategy, you're quoting maker orders on one venue and hedging with taker orders on another. The edge is the spread dislocation between the two. The problem: not all fills are equal. Some fills happen because random noise pushed the spread wide enough for your signal to trigger. These are clean fills. The edge holds through your hedge execution, you capture the dislocation, everyone's happy. Other fills happen because an informed participant, someone who knows where price is going next, deliberately takes your resting liquidity. They fill you because your quote is mispriced relative to information they have. By the time your hedge leg executes 100-500ms later, the edge has evaporated. Sometimes it's gone negative. This is toxic flow. You got picked off. The insidious part: both fills look identical at the moment of execution. Same spread, same signal, same z-score. You can't tell them apart by looking at your entry conditions. The difference only reveals itself after the fact, when you measure how much edge survived through hedge execution. For stat arb specifically, this is devastating because: Your maker leg sits in the order book advertising exactly where you think fair value is. Every informed trader on the venue can see it. When they know price is about to move, your quote is the cheapest liquidity available. You become the exit door for someone else's alpha. The faster and more informed the flow, the worse it gets. Your fill rate might look great, but your PnL doesn't match, because you're systematically filled on the wrong side of information events. So how do you defend against it? You need to predict whether the next fill will be toxic BEFORE you get filled. Not after. Not during. Before. This means reading the microstructure of the order book in real time and recognizing the patterns that historically preceded bad fills. Then deciding whether to even have your quote live at that moment. Here's what our engineering team is currently building and integrating, a full toxic flow detection and prevention framework: Order Book Microstructure Signals The order book is not static. It's a living structure that changes shape before major moves. We're tracking: Book imbalance at best bid/ask: the ratio of resting size at the top of book on each side. When you're quoting a buy and ask-side depth massively outweighs bid-side depth, that's adverse. This is the single highest-value predictor of toxic fills. Depth-weighted imbalance across multiple levels: same concept but exponentially weighted across the top 5 levels. A thin bid side with stacked asks 2-3 ticks deep is a stronger signal than just level 1. Imbalance rate of change: static imbalance matters less than accelerating imbalance. If bid depth is draining over the last 200ms to 1 second, that's a momentum signal the book is about to move through your level. We track the delta across three lookback windows. Spread compression and expansion dynamics: if the spread is tightening toward your quote, more participants are competing. Tight spreads on Hyperliquid tend to precede directional moves. We track spread in basis points and its short-term velocity. Order arrival and cancellation velocity: counting new orders placed and cancelled per unit time on each side. A spike in cancellations on your side of the book is a strong adverse selection signal. Other makers are pulling their quotes. They know something. Queue position erosion: if orders ahead of you in the queue are being cancelled (not filled), your effective queue position improves. Paradoxically this is dangerous. Informed makers are withdrawing, leaving your quote as the last available liquidity. Trade Flow Signals Beyond the static book, the stream of actual trades tells a story: Recent trade direction and intensity: classifying trades as buyer-initiated or seller-initiated and computing signed volume over trailing windows of 1, 5, 15, and 60 seconds. Heavy one-directional aggression preceding your quote is the classic toxic setup. Trade size distribution analysis: informed flow tends to come in specific size clusters. We profile historical toxic fills by aggressor order size and flag when incoming sizes exceed 1.5 standard deviations above the rolling mean. Trade arrival rate deviation: under normal conditions, trade arrivals approximate a Poisson process. When inter-arrival time drops significantly below the expected rate - a burst of trades - it often indicates informed flow or a liquidation cascade. Volume-weighted price momentum: short-term VWAP slope over recent trades. If VWAP is trending against your quote direction, the edge is decaying before you even get filled. Aggressor repetition tracking: if the same address is repeatedly taking liquidity on one side in quick succession, that's likely an informed participant. Concentrated flow from single wallets gets flagged. Cross-Venue and Cross-Provider Signals For stat arb, the relationship between venues is critical: Price dislocation velocity: we already compute cross-provider spreads. But the speed at which dislocations close tells you about information content. If the dislocation you're arbing is closing rapidly before you get filled, the move is information-driven, not noise. We track the half-life of recent dislocations per pair. Lead-lag relationship shifts: identifying which provider currently leads price discovery. If the venue where you're quoting maker is lagging, your fill is more likely toxic because you're being picked off by someone arbing the same dislocation faster than you. Funding rate and its derivative: on Hyperliquid perps, funding rate changes reflect positioning imbalances. Rapidly shifting funding signals directional pressure building against your quote direction. Basis dynamics: tracking basis shifts between the perp you're quoting and correlated instruments. Accelerating basis movement adverse to your quote direction is informed flow repricing the market. Correlated asset moves: BTC and ETH move first. Alts follow. We track real-time price changes in major assets as leading indicators, computing beta-adjusted expected moves for the asset we're quoting. Volatility Regime Detection High-volatility environments have structurally more toxic flow because price moves faster than your hedge leg can execute: Realized volatility regime classification: rolling realized vol over 1-minute, 5-minute, and 15-minute windows. Above certain thresholds, we widen edge requirements or stop quoting entirely. Volatility of volatility: sudden vol spikes are more dangerous than sustained high vol, because the model is calibrated to the prior regime. We track if realized vol just jumped more than 2 standard deviations from its own rolling mean. Implied volatility proxy: using the width of market maker quotes as a proxy for expected vol. When spreads across the market suddenly widen, it signals a regime change. Fill-Specific Forensics Your own fill history is training data: Time-to-fill analysis: orders that get filled very quickly after being placed are more likely toxic. Immediate fills mean someone was waiting to pick you off. Orders that rest before filling tend to be noise flow. We build Bayesian priors from the distribution of fill times for toxic vs clean fills. Fill size relative to quote size: full instant fills are more toxic than partial fills. Full fills suggest the aggressor specifically wanted your liquidity at your price, implying they believe it's mispriced. Position in aggressor sweep: if your fill was part of a larger sweep across multiple price levels, you were the first stop on a directional move. Timing and Temporal Signals Time since last major price move: mean reversion vs momentum detection. If the dislocation appeared after a sharp move that's less than T seconds old, there's higher probability it continues. If it's been stable, it's more likely noise-driven and safe. Liquidation cascade detection: liquidations create forced directional flow. Sharp price move combined with high volume and specific size patterns. Avoid quoting into cascades. Time-of-day effects: certain hours have structurally different flow toxicity. US market open, Asian market open, major macro events. Profiling historical toxic fill rate by hour and day. Event proximity: CPI, FOMC, token unlocks. Flow becomes dramatically more toxic around scheduled events. Widening thresholds or stopping quoting within proximity of known events. Hyperliquid-Specific Intelligence Open interest changes: rapid OI increases suggest new directional positions being opened. OI decreases suggest closing, potentially mean-reverting. Tracking OI delta per unit time. Known address classification: building a database that classifies Hyperliquid addresses we've been filled by as toxic or non-toxic based on historical outcomes. Over time this becomes the most accurate signal. You literally know which counterparties are informed. The Model Architecture All of these signals feed into a feature vector updated on every order book change. Every fill gets labeled against a pair-aware adverse-selection threshold: toxic if the realized edge at fill drops below 50% of the pair's expected bypass edge. We train gradient-boosted trees offline on the labeled dataset with time-based splits to avoid lookahead bias. The cost function is asymmetric: false negatives (toxic fills you didn't avoid) cost real money, false positives (clean fills you skipped) cost opportunity. We tune the threshold to minimize expected cost, not accuracy. The goal is not to trade more. It's to stop trading at exactly the moments when the next fill will destroy your edge.

imagine not needing to care about oil volatility and exploding funding rates while farming volume and profits

We might not have the most users, but maybe the happiest? Market yesterday was pretty active = elevated volatility = big profits for our users.

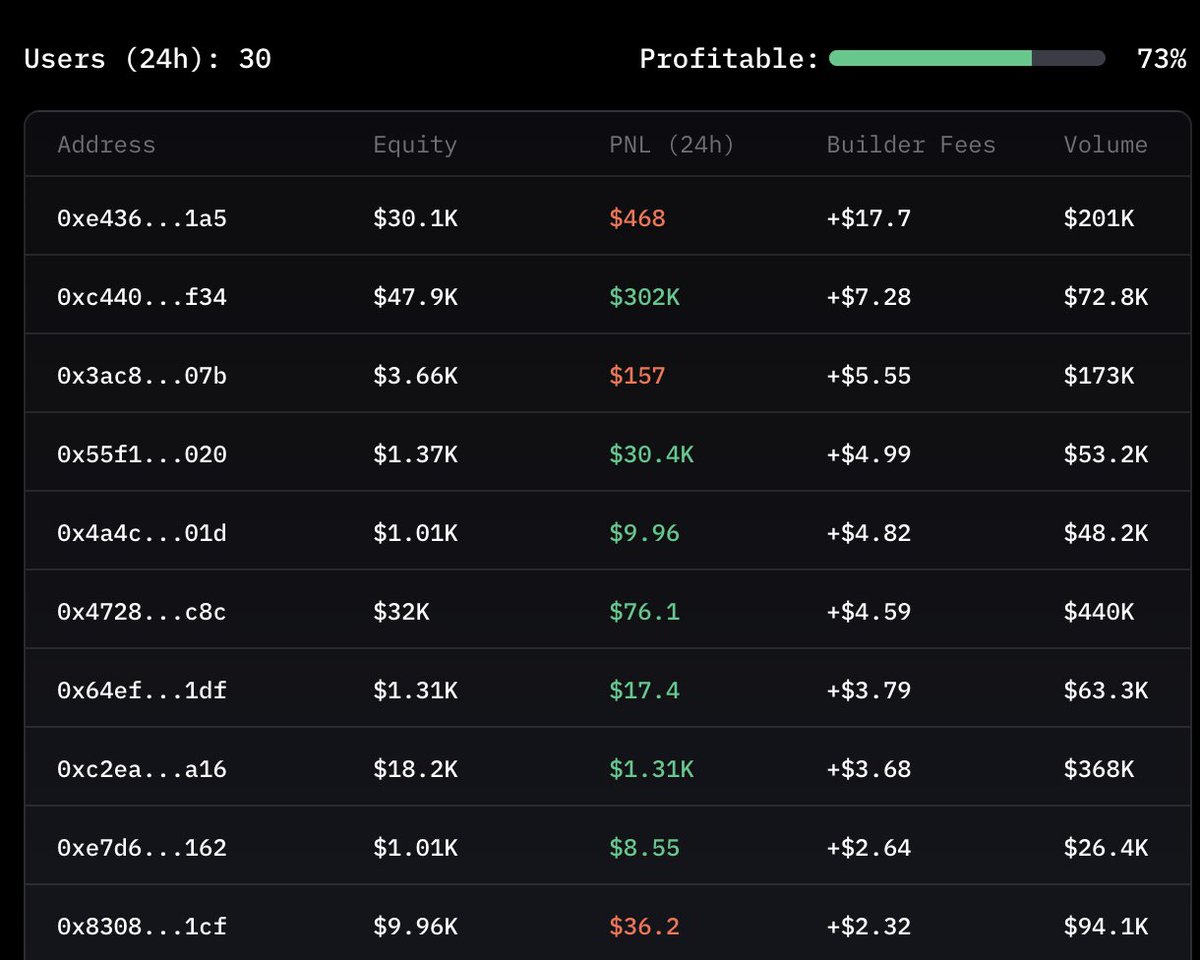

day 4 on hyperliquid in the books and a new ATH record of 82% of users in profit in the last 24 hours. can you find any other builder on @HyperTracker that comes close to this? it's usually hard to find anything above 35%... try it out right now and farm all HIP3 @Dreamcash (+$USDT rewards), @tradexyz, @markets_xyz and @felixprotocol with our stat arb algo. stop burning a "budget" to farm volume, start earning via positive PnL and consider points as a bonus

he's not wrong

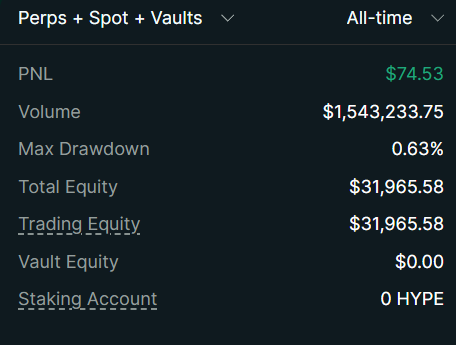

Y'all are dumb Y'all burn money on Hip3 I'm using @PlanemoTrading's HIP3 Stat ARB bot for 50% APR + Hip3 volume! 👉planemotrading.xyz/?ref=XPGBJ3H6DG 👈 (10% point boost) My 2 day results=$1.5M Hip3 Volume+$75 P&L -Spreads the algo trade include $AMZN, $META, $INTC, $CL, $BRENTOIL,

day4 on @HyperliquidX so far looking very solid we measure farming not in cost per million, but in profit per million btw wen custom logo and info for our builder @HyperTracker

Another goated trade. This guy just farmed $80k @tradexyz volume in 5 minutes and made $45 profit on top. Stop using inferior platforms where you lose ABSURD amounts of money per $1M/volume ($200 - 700 often) and try out our stat arb algo: hip3.planemotrading.xyz

Day 3 on @HyperliquidX doing stat arb on @markets_xyz @tradexyz @felixprotocol @Dreamcash 74% of users profitable today (including builder fees). The market drop in the evening led to some great entries & exits. Volatility = we print even more

Get started today and farm @HyperliquidX and HIP3 with a positive PnL: x.com/PlanemoTrading…

what is statistical arbitrage and why we built an algo around it. stat arb is one of the oldest strategies in quantitative finance. it originated in the 1980s on morgan stanley's equity trading desk and has been a core strategy at hedge funds and prop firms ever since. the

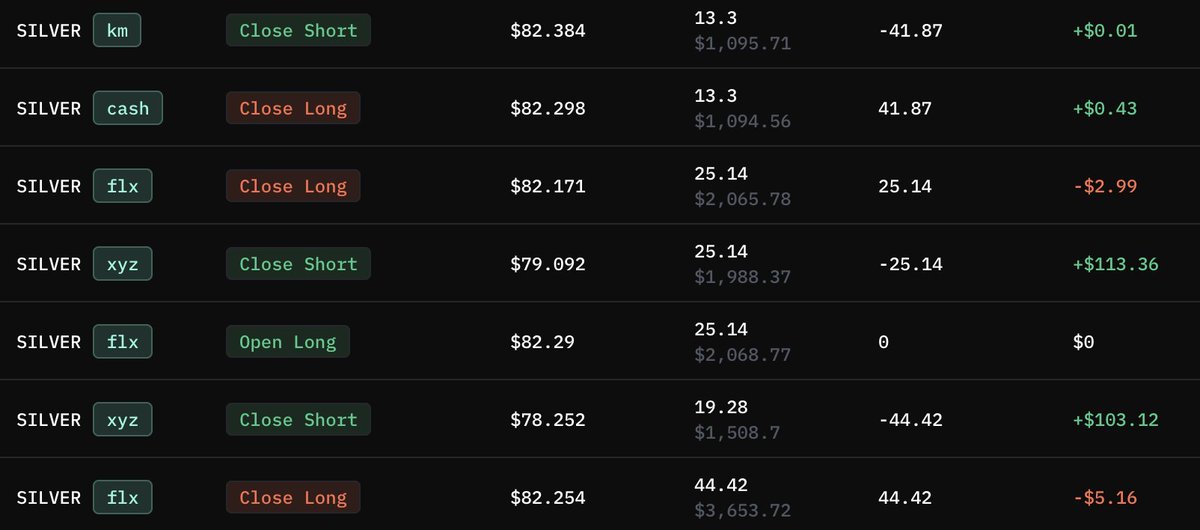

2) What happens normally is that one leg exits at a loss, while the other exits at a profit, and the net amount is positive. But things sometimes look different, especially if you have a strong tailwind in form of great entries. Great entries often let you exit both legs at a profit, as in the example below.

We've been live on Hyperliquid for 3 days now. Time to highlight our favourite trades our stat arb algo executed for our users. 1) By far the best one, is this crazy SILVER trade that happened on Friday. Big dislocations on the SILVER @tradexyz and @felixprotocol market there, +$200 within a few minutes. (We usually are happy to exit a trade with a few bps of profit). The $200 here translate to a few % on the user's collateral.

Lovely. Great entries allow for a profitable exit on both legs from time to time.

CL (xyz) - BRENTOIL (xyz) statistical arbitrage is now live on @PlanemoTrading. Farm double the volume on @tradexyz compared to our usual pairs. hip3.planemotrading.xyz

Shakawat Hosen @dowlat6520

1K Followers 3K Following Building strong Web3 communities. Engagement , Moderation , Growth , Support. Angel of @CoinWOfficial. Ambassador @xomarket Contributor/Builder on @inkonchain

umibeatz @umibeatz

935 Followers 6K Following . . StakeOutRadio @stakeoutR on @subfm Mon 9-12pm (ET)

jay @0xmasterjay

256 Followers 3K Following Attorney. Terrible Trader. Crypto nerd. Hot-take enthusiast.

Mad Journalist 🗞�... @yekaza123

3K Followers 2K Following Perpdex maxi |Airdrops and alphas | Trading signals from the best indicator itw 📈|All my contents are for education NFA,DYOR |Collabs DM open 💌|

Ali.eth 🐬 @aliwev3

213 Followers 309 Following Learning About Blockchain and Cryptography || praxis Nomad

ShiraiFromBasement @only_shirai

359 Followers 311 Following 七転び八起き| Detrenchification | He that is Him

cryppi / perpdexlist @cryppimagic

4K Followers 2K Following No CEX on the first date; @perpdexlist founder

✪ @Lord0fAllts

13 Followers 352 Following Educational Content. There're No Absolute Just Probabilities. You Just Need One Cycle To Make It All.... Show more

Taker @0xTaker

3K Followers 3K Following market microstructure kind of guy. mev https://t.co/1zA6rJJ2r0

Aiman @aimantian999

250 Followers 7K Following Keep Building #BNB #BTC|Binance 4.6亿用户选择https://t.co/qByENtBqK9|合作Dm Tg|Co-Founder of Aiman Capital|All in Crypto & Web3.

Elex ($/acc) @elex5739

341 Followers 3K Following Crypto games. Wiz @BTC_WizOrds Citizen @yama_wrld @playmadworld (🧙♂️,🧙♂️) gnoma

Dark Fortuna @MgFrtn117

27 Followers 635 Following

tvanleiden 🌴 ☀�... @tvanleiden

771 Followers 4K Following Dreaming a CypherPunk Artificial Island on International Waters.

StarCall @starcall_it

9 Followers 56 Following Connect with you favorite creators through quality video calls, pay with Solana or Stablecoins (only devnet for now)

Ivan Gen @0xIvanGen

39 Followers 213 Following Ex-Investment Banker. Started with stocks, discovered crypto 🪙 | Now exploring the wild world of Web3 | Here to learn, share & grow together 🌱

Andre Yun @AndreiUn1709

2 Followers 15 Following

ositoninja @ositoninja1

1K Followers 2K Following

Galeo Alpha @GaleoAlpha

7K Followers 6K Following Kripto Para Analisti | Piyasa Trendleri & Stratejiler | Güncel Haberler | Yatırım Tavsiyesi Değildir | Since 2017

Troyster⚡️| π² @0xtroyster

1K Followers 7K Following Crypto | Investor | NFT Holder | Content Writer | Meme | Visual Art | AI | BASEMAXI | 🇹🇭 | NFA

DoN @0x_DoNjayy

5K Followers 3K Following re•building for the Golden age of creativity | content creator | clipper

Mossad Crypto inst. e... @TheMossad_0310

1K Followers 1K Following Crypto entrepreneur, blockchain enthusiast, understanding that decentralization in crypto is a utopia.

Treva @Treva37396044

202 Followers 211 Following Turning dreams into plans. | Adventure seeker | Coffee enthusiast ☕

zkMurton 🌞 @Mirton70567512

277 Followers 2K Following От хаосът правим форма! /// Also Elite @EigenTribe @eigenlayer https://t.co/5arU09nSSl

MAB! @MeharBela

1K Followers 6K Following Alive! | Software Engineer 👨💻 | Optimizing Life And Business Through Tech. 💻 | Digital Marketer | AI & Web3 Enthusiast 🌐

G.M.🕯️ @GjulnazM

60 Followers 218 Following Visual storytelling & worldbuilding, AI-assisted, idea-led✨ QA Engineer | Web3 testnets & UX bug reports 📱💻

Dunnaz 🔳 (△/acc) @DunnazFlow

2K Followers 974 Following Fundamentals | Price action trader | order flow, statistics & education | Day Trader Zero Fee exchange - https://t.co/28jUzhj80i

Andrεω ☜ @SWEATY333

23K Followers 9K Following ✞. Meme Warlord ⚔︎ || Rebuilding The Original Meme Generator of the Internet ⬎

BaseMessiah @0XBaseMessiah

259 Followers 88 Following Fixing broken content distribution systems for brands and apps | Sports Prediction markets arc

Toronto @torontoErdem

12K Followers 2K Following Valorant player Former: @OXG_Esports @misaesports @NOM_Esports @IWcats @FormulationGG 深呼吸 Getting some fun via crypto

nolan.snr 〽️ @nolansnr_098

6K Followers 989 Following Onchain enjoyer | 90% stablecoin | 10% $btc $eth $bnb $sol | perpetual and gamble market maxi

Achak @WolfAchak

123 Followers 131 Following "If you live among wolves you have to act like a wolf." always debunking shit posted by other !!

kate_crypto_相互 @qbicrube10s

113 Followers 673 Following web3系の発信をしていけたらと思っています!有益な情報を発信していきますので、フォロー頂けるとありがたいです!

Por | DeFiSecret @defisecret

4K Followers 786 Following Full Time Crypto Analyst | Ambassador: @Cloud | TG Group: https://t.co/jHZDEzbC8w | Thai Blog: https://t.co/qkIBCtRgUS

uub @uubdik

76 Followers 2K Following

Jincoz @Jincoz

4K Followers 4K Following In the midst of chaos, there is also opportunity || Building @SkyverseHQ || @PortarcHQ enjoyer

fiveup-man @fiveupcoin

378 Followers 527 Following Cuisine | Travel | Culture | Motorcycle | Stock Market VietNam | Vietnamese

AngryKong @angrykong48

291 Followers 905 Following Crypto & markets. World events. Fitness. BJJ. Fatherhood. Discipline. Stand for what’s right.

will @nicsickwilly

101 Followers 2K Following fuzzy dark matter stuff, margin prediction market stuff @LatticaFinance

Chris @C_AKuma31

78 Followers 479 Following Développeur Web ( Javacript - Nodejs- Reactjs - Vuejs- SQL - MongoDB ) Bourse | Blockchain | Immo

Mad Journalist 🗞�... @yekaza123

3K Followers 2K Following Perpdex maxi |Airdrops and alphas | Trading signals from the best indicator itw 📈|All my contents are for education NFA,DYOR |Collabs DM open 💌|

Mossad Crypto inst. e... @TheMossad_0310

1K Followers 1K Following Crypto entrepreneur, blockchain enthusiast, understanding that decentralization in crypto is a utopia.

Aoke Quant 奥克队�... @aoke_quant

10K Followers 3K Following 17年进圈躺平型量化交易者🚩七年币安队长服务超千人专业返佣🏆币安最佳金算盘奖、长青伙伴奖。 前大厂程序员|Ai|Defi|套利|投资&投机|平时瞎哔哔|偶尔干货|爱好旅游已打卡两次🇺🇸旅居 #Binance 币安注册使用【Y1OQZ8OD】码注册账号🤖免费体验量化策略🧧注册前私信免费开通子账户功能👇

ABDE @ixAbdeRabbi

851 Followers 5K Following Web3 & Crypto Strategist | Founder & Builder || Formerly @ KuCoin, Currently Growth Manager @PokepayGlobal & CMO @OpenCryptoCom

STELLAR INSIGHT NETWO... @DustoAlif9

241 Followers 2K Following

Whitelist Media @Whitelist1Media

30K Followers 1K Following Leading CIS Crypto Media & Community. Web3 insights from Telegram to X Marketing Arm: @Whitelist1Agncy

joeiiix (evm/acc) @duychiphs

355 Followers 2K Following UI/UX Designer | more than 5yrs exp NFT OG | Gamefi | Crypto Farmer ETH Maxi

Atreus @Astreus_5

3K Followers 3K Following Building the future with AI & Web3 • Content Creator • Daily Discipline • @realmadrid✨

NoVa @NoVaLeVrai1

771 Followers 1K Following Buy only fear shows up in the market. In the end we will be right. At 200% 🧠

Datweb3guy @Datweb3guy

8K Followers 6K Following Building | Community Management | 1x hackathon winner | Onchain Analyst - helping Projects Build Dune Dashboards and Analysis

webed IP @emontig

248 Followers 2K Following

Trends for United States

You might like