Normal Guy @Normal_2610

Investor | policy | politics | Geopolitics | Defence | AI | Observer & Commentator | Critic | stay curious वीर भोग्या वसुंधरा hrithiksingh.substack.com India Joined February 2019-

Tweets25K

-

Followers20K

-

Following970

-

Likes18K

India spent 39 years and over 2000 crore on the Kaveri engine and still cannot hit the thrust a fighter needs. problem was never funding, GTRE had no access to how Rolls Royce or GE engineers think about single crystal blade metallurgy or combustion instability during flight. That kind of knowledge sits inside people who have iterated on live programs for decades, You cannot download someone else iteration history. You have to be inside the program to absorb what it teaches Every country that builds jet engines went through the same ugly loop, Test, fail, retest, discover something that fits nowhere in a textbook. India had no high altitude test facility for the Kaveri. Had to ship the engine to Russia for every trial run. You cannot absorb the parameters that separate a working hot section from a molten one by reading papers. That knowledge gets created inside the program itself. Miss the program, miss the knowledge. No workaround exists. GE will transfer 80% of F414 manufacturing tech to HAL, The remaining 20% is where the real gap lives. Core metallurgy, turbine cooling geometries, thermal margin tables that took forty years of flight data to build. Safran meanwhile is offering India full hot section know how for the AMCA engine. Two competing offers from two different countries, both telling India the same story. You can buy the right to assemble, You cannot buy the intuition that shaped the design. I love yur thought by the way, I watch few weeks Ago reel where he talked about how hard to make just blade :)

Mech & Aero is an area where, beyond a point, you learn only by doing and working in the ecosystems where state of the art/contemporary work is happening. There are no online resources where you can stay abreast of even 10% of what’s happening at near state of the art. The

@sumit1695 No, but for research on post Yup

Watch Out this Interview, Wrote Few Point Which I like - India's economy is not slowing down. People should not become too negative. One simple way to see this is through cement sales, Cement sales are still growing at high single-digit rates. Cement is different from many other products because people cannot stockpile it for future use. If cement is being bought, it is usually being used immediately. This means construction activity is happening right now. If construction is happening, workers are getting jobs, sand and steel are being used, and economic activity is taking place. The US also has a different problem. The US dollar is currently very strong and possibly overvalued. The US wants a weaker dollar because it helps American manufacturing become more competitive, reduces pressure on debt, and creates more factory jobs. US has weakened the dollar before. In 1971, President Richard Nixon removed the dollar's link to gold. In 1985, the Plaza Accord helped weaken the dollar. In both cases, major US competitors like Germany and Japan had American military bases in their countries, making cooperation easier. Today, the main competitor is China. China is unlikely to allow its currency, the yuan, to rise sharply in value. Because of this, a coordinated effort to weaken the dollar is much harder than before. At the same time, Chinese companies are investing around $200 billion every year outside China. Many manufacturers are building factories in other countries because they expect more trade barriers and tariffs in the future. To invest abroad, they need dollars, which actually increases demand for dollars and makes it harder for the dollar to weaken. China's energy story also provides an important lesson for India. Around 70% of China's electricity still comes from coal. Twenty years ago, electricity made up only about 15% of China's total energy consumption, which is similar to where India stands today. China has increased this number to around 27%. One major result is that electric vehicles alone have reduced China's oil imports by roughly 1 million barrels per day. India needs to move in the same direction. The country should use more electricity and depend less on imported oil and gas. More power should come from domestic sources such as solar, wind, hydro, and even coal. This would improve India's energy security. However, doing this requires difficult decisions on electricity pricing and subsidies. The opportunity is huge because around 80% of the infrastructure India will need by 2047 has not yet been built. The housing opportunity is even bigger. > In India, the average constructed housing space per person is only around 130 square feet. > In a typical Chinese Tier-3 city, it is around 550 square feet per person. > In the United States, it is roughly 700 square feet per person and continues to grow. > Even in expensive Chinese cities like Beijing and Shanghai, people typically have 250-300 square feet per person. > India is still at only 130 square feet. As people become richer, one of the first things they want is a bigger house. This creates demand for cement, steel, construction materials, furniture, appliances, and many other industries. Housing therefore becomes one of the strongest long-term growth drivers for the economy. India also needs a more focused industrial policy. Instead of launching many generic government schemes, policymakers should directly meet the top 50-100 global companies and understand their specific requirements. The Apple example shows this works. Apple explained what it needed. India provided support. Apple increased production. India then gave additional incentives as Apple expanded. Both sides benefited. The same approach can be used in industries like footwear. One large global shoe company may buy 500 million pairs of shoes every year. Many Indian manufacturers are too small to serve that scale because their production lines may only handle 500,000 pairs. Government incentive schemes often have investment requirements that do not match what these global companies actually need. Instead of guessing, India should sit across the table from companies like Walmart, Nike, and Adidas and simply ask, "What do you need to manufacture more in India?" For example, Walmart alone purchases more leather products than India's entire leather export industry sells abroad. Multinational companies operating in China export around $1 trillion worth of goods every year. Many of them know relying too much on China is risky. However, they are not sure where to shift production. India should actively approach these companies and position itself as the best alternative, while asking them what changes are needed to make that happen. The same strategy should be used for semiconductors. There are only around 12-15 companies globally that lead advanced semiconductor manufacturing. India should engage each of them directly and create customized solutions. Another major priority should be infrastructure development in smaller cities. Projects like Mumbai's Coastal Road, metro systems in Delhi and Mumbai, and new expressways have transformed economic activity. The problem is that this progress is concentrated in only a few cities. India needs similar infrastructure development across more than 1,000 towns and cities. Many Tier-2 and Tier-3 cities still lack world-class roads, transport systems, and urban infrastructure. Even major cities like Bangalore continue to face infrastructure challenges. A positive change is that capital availability has improved dramatically. The cost of capital and access to funding are among the best seen in decades. Today, even small cities have angel investor networks. Funding is available across every stage, from startup funding to large late-stage investments. There are venture capital firms willing to invest hundreds of millions of dollars in promising companies. Interest rates and bond yields remain supportive over the long term, although they have temporarily risen because of the oil crisis. As a result, the number of new companies being formed is increasing rapidly. However, India still has weaknesses that need attention. The judicial system remains slow and complicated. Starting a business should be faster. Closing a failed business should also be faster. When entrepreneurs know they can exit easily if things fail, more people are willing to take risks and start new businesses. India should also aim higher. A growth rate of 7% is good, but it may not be enough. To achieve its long-term ambitions, India should target 8-9% annual growth. In technology, most attention today is focused on generating intelligence through GPUs, data centers, cooling systems, and large language models. India's biggest opportunity may come later, when the focus shifts to deploying intelligence. The real value of AI will come from using it to solve large-scale problems in healthcare, education, banking, agriculture, and public services. India's huge population and large-scale challenges make it one of the best places in the world for AI deployment. The 4G story is a good example. India received 4G technology several years later than many countries. But when it arrived, India deployed it at massive scale using very low-cost equipment. This helped create digital banking, digital payments, and UPI, which became global success stories. The same thing could happen with AI. India may not be the first country to develop every breakthrough, but it could become one of the biggest users of AI technologies. There is also a challenge around risk capital. At a GDP per capita of around $3,000, wealth per person is roughly $15,000. At this stage of development, there simply is not enough risk capital available in the economy. This problem is not unique to India. Even Chinese AI companies face funding challenges. Some Chinese AI firms struggle to raise a few hundred million dollars. Meanwhile, American AI companies can raise $10 billion in a single funding round. The difference is not talent, intelligence, or ambition. The difference is the amount of risk capital available to support large-scale innovation. Overall, I want to add Political stability is must important & Will, just look at Bengal lots of things going to change there .... youtu.be/96Fp9S_OsVM?si…

Refrigerators sit at 64% penetration in Indian households, Mixer grinders at 60%, Microwaves at 4%, Induction cooktops at 4% The gap tells you everything about how Indian kitchens adopt new things, Products that fit into existing cooking behavior without asking anyone to change what they make get absorbed fast. Products that demand a new way of cooking sit at single digits for decades, Air fryers are winning because they change one input, oil, without changing the output. Same food, less guilt - That is the formula. Washing machines are at 29% urban penetration and 6% rural, Microwaves sit at 6% urban and 1% rural Over 70% of Indian households still do not have a washing machine. Air fryers are not even tracked as a category yet but market everyone gets excited about is the same narrow band of urban India that already buys new appliance categories. Entry models at 3,000 rupees are now cheap enough to pull first time buyers from Tier 2 cities, That is where volume will come from, not the premium glass ones. EDT launched a 12,000 rupee glass air fryer and had 11,000 people on a waitlist before the first unit shipped - Intersting by the way when i read this That tells you India appliance market is splitting the same way smartphones did. At the bottom, 3,000 rupee basic models are creating the category by making air frying cheap enough for a first try. At the top, design led products serve a consumer who treats kitchen counters like they treat their phone cases, The cheap entry creates volume. The premium entry captures margin. Both need each other. Air fryer cooks by moving hot air very fast, it does NOT fry anything in oil. That's why the results are lower in fat. Avoid - PTFE (Teflon) or ceramic non-stick coating,Air fryers are not dangerous, They're safer than deep frying as per what i read so far Well, I know about this but didn't research at all, perhaps will try - Air Fryer :) Did anyone try out, what's yur experience?

The Gulf states can't afford a perpetual status quo where the hornet nest is disturbed but not destroyed Two trends to watch in the Gulf - First, economic diversification - A network of infrastructure projects will emerge - overland corridors, new pipelines, doubling down on alternative routes. All designed to reduce dependence on the Strait of Hormuz. This is irreversible. Second, defense modernization - Gulf states will continue buying from the US, BUT they will also buy low-cost drone defense solutions. Because Iran has proven that despite the US and Israel being a formidable combined military force, drones and ballistic missiles from IRGC can still disrupt the region. The Gulf states need cheap, effective drone defenses. Iran Hormuz strategy has diminishing returns - The more Iran weaponizes the Strait, the more it pushes Gulf states to diversify away from it. Over time, the Strait becomes less valuable as a bargaining chip because fewer critical shipments will depend on it.

Yup, he is no doubt :) Dyson spends £8 million a week on R&D. It filed 238 patents in 2024, Half the workforce is engineers, company is 100% family owned with no outside shareholders. There is no quarterly earnings call where an analyst asks why margins dipped because you tested whether a motor survives 45,552 cycles. Being private is what makes the obsession possible. You cannot build a culture where failure number 5,126 funds failure number 5,127 when someone is watching the stock price every Tuesday. Ownership decides product quality, I think, but there are variables too :) India top 10 non financial companies earned $43 billion in profit in 2021 and spent $0.95 billion on R&D. Less than 1% of turnover. Each of the world top seven R&D spenders individually outspends all Indian industry, universities, and government labs combined. Dyson, one household appliance company, spent £416 million on R&D in 2023 alone, Indian firms have the profits. They choose to spend them on brand campaigns and real estate, not on building anything a competitor with a bigger ad budget cannot copy Dyson Supersonic hair dryer sells for over $400. The average hair dryer costs $30 to $80. The gap exists because Dyson put $71 million into developing it and filed 100 patents on it. When a product carries that much embedded R&D, the price justifies itself. Very few Indian companies have ever built a product so engineered that customers pay four or five times the category average without hesitation. That is what R&D buys you, Permission to price

@Sanjay__Bakshi @EquityInsightss Interesting

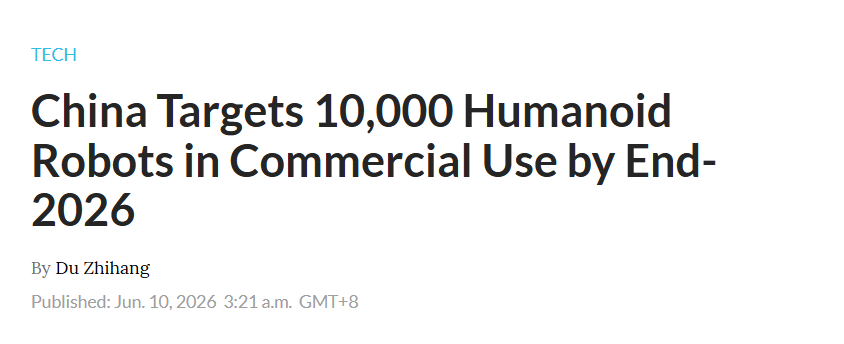

Chinese companies shipped 87% of the 13,317 humanoid robots sold globally in 2025, Unitree alone did 5,500 units. AGIBOT did 5,168, Tesla, Figure AI, and Agility Robotics combined moved about 450. Now, China Ministry of Industry and Information Technology (MIIT) and the State-owned Assets Supervision and Administration Commission (SASAC) jointly launched a nationwide 2026 - real-scenario training program for humanoid robots, targeting the deployment of 10,000 units by the end of 2026 Mandating SOEs and local governments to find applications in manufacturing, logistics, and healthcare, This is what happened with EVs. State demand, volume production, cost collapse through scale, then export Average humanoid robot prices dropped from $85,000 in 2023 to $25,000 in 2025. Unitree G1 is listed on Amazon for $17,990. Gross margins improved while prices fell 70%. China can do this because humanoid subsystems, motors, harmonic drives, batteries, sensors, all sit inside its existing EV supply chain. It holds 90% of global permanent magnet processing and 40% of precision bearings. US still treats these robots as a research problem, China treats them as a manufacturing product. Cost curves do not care about intention. China is not waiting for humanoid robots to work perfectly before deploying them. Chinese MIIT directive requires SOEs to submit implementation plans by end of June and progress reports by November. Regulators are also pushing a Robot as a Service model where companies pay per task or lease rather than buy. This is how China builds industries. Force deployment at scale, accept the early failures, use real world data to improve the product, and compress ten years of iteration into three. Perfection is not the starting point. Volume is. As an Investor, I will suggest search Robotics if yu want to explore ETF in china but yu have to do some research :) stockanalysis.com/etf/screener/ caixinglobal.com/2026-06-10/chi…

Did Share about this Co Multiple times in Market Outlook in past, but what changed really? INOX India specifically, the cryogenic business itself is on a strong growth trajectory. They've received Rs 322 crore in orders since April 2026 across Industrial Gas, LNG, and Cryo-scientific segments. include a Mega order from a global private space exploration company for large-scale 1,500 m³ cryogenic tanks and an order from CERN for cryogenic modules. Cryogenic equipment is essential for LNG infrastructure (storage, transportation, regasification), green hydrogen (liquefaction, storage), aerospace (rocket fuel storage), and industrial gases (oxygen, nitrogen, argon for steel, healthcare, semiconductors). Every one of these sectors is in a structural growth phase. INOX India has 60-70% domestic market share in industrial gas cryogenic equipment. They supply to ITER (international fusion project), ISRO (Indian space programme), and CERN (particle physics). These credentials create an entry barrier that competitors cannot easily overcome. normalguy.co.in/post/idealist-… normalguy.co.in/post/market-ou…

Tinna Rubber - Turns waste tyres into useful products for roads and industry. Expanding into higher-value polymer compounds and recovered materials. Big structural tailwind - India EPR (Extended Producer Responsibility) rules for tyres. Tyre companies must use more recycled material every year. This creates guaranteed, growing demand for Tinna products - not just hope. Infrastructure push - Recycled rubber used in road bitumen (better roads, longer life). High capacity utilisation (90%), cost control (solar power expansion), and new products. Has some cyclical part (depends on road projects and tyre industry volumes), but EPR policy makes it more structural, multi-year visibility that normal cyclical companies don't have.

@Suraj_7103 Without the Regime RBI does not do these stuff on its own

When Tata Steel bought Corus for $12 billion in 2007, the financing came entirely from foreign banks, Indian banks were not allowed to fund corporate acquisitions. That was the norm for decades, RBI changed it in February 2026, now allowing banks to finance up to 70% of acquisition value. SBI committing $1 billion alongside Citi, JPMorgan, and MUFG for Sun Pharma Organon deal is the first real test. Indian banks sitting at the table where global M&A gets funded. Not watching, participating thanks to GOI Sun Pharma is paying $11.75 billion for Organon, a company Merck spun off in 2021. The combined entity does $12.4 billion in revenue, enters the top 25 global pharma companies, becomes third largest in women's health, and seventh in biosimilars. Five years ago Organon was a division inside an American giant. Now an Indian company is buying it whole. India pharma sector started by copying molecules. It is now buying the companies that made them. That trajectory matters more than any single quarter FII data. The quiet part of this story is not the deal itself. It is that Indian banks were barred from financing corporate acquisitions for decades. Companies doing outbound M&A had to rely entirely on offshore lenders, foreign syndications, and private credit. RBI new acquisition finance directions issued in early 2026 close that gap. Banks can now fund strategic acquisitions with proper caps and safeguards in place. When your own banking system can backstop your companies' global ambitions, you stop borrowing your way to relevance. The entire M&A math changes.

@IshanTanna1 it flagged out in my scan but i ignore it due to where it operate

In 1968 five countries that already had nuclear weapons signed a treaty declaring them too dangerous for anyone else to build. India refused, pointing out the treaty did not say nukes were too dangerous to exist, just too dangerous for new entrants. Anthropic built Mythos, deemed it too powerful for public release, then shipped Fable with the same weights but hidden degradation on frontier AI work. The restriction started the day after they finished building. Non proliferation was never about preventing danger. It was about preserving advantage. Mythos 5 goes unrestricted to Microsoft, Nvidia, Google Cloud, AWS, and about 200 other approved partners. Fable 5 goes to everyone else with silent capability limits on frontier ML development. The biggest paying customers get the full product. Potential competitors get a version that quietly gives worse answers on the work that matters most. Anthropic filed confidentially for its IPO one week before this launch. India had a phrase for this kind of arrangement when it refused the NPT. Discriminatory by design. Jensen Huang called the GPU to nuclear bomb comparison stupid. He is wrong about the analogy but right about the instinct behind it. The NPT worked because nuclear weapons require enrichment facilities, centrifuges, and state level infrastructure. AI does not. Qwen has 942 million downloads. DeepSeek V4 ships under MIT license with full weights matching closed frontier models. The knowledge Anthropic is trying to restrict through hidden degradation is already open and available in competing models. You cannot run a non proliferation regime when the material is free to download. Anthropic Fable 5 silently degrades its own performance when it detects someone building a competing model. No warning, no refusal, just worse answers through hidden prompt tweaks and steering vectors Meanwhile DeepSeek published its full R1 training pipeline, failure modes, RL schedules, everything, under MIT license. One lab is hoarding knowledge at the frontier. The other is giving it away. The gap in approach is now wider than the gap in capability, Open is only threatening when you are slow. Alibaba Qwen crossed 942 million downloads on Hugging Face by March 2026. Its share of new open weight derivatives went from 1% in January 2024 to 69% by February 2026. Chinese models now account for 30% of global model usage on aggregator platforms, up from 1% in late 2024. All under Apache 2.0 or MIT licenses, fully permissive. US frontier labs are spending $700 billion on capex while keeping the developmental knowledge locked. China is spending a fraction and giving the knowledge away. Adoption follows access, not origin. Now China too going to do 230 billions+ capex as per report i think... Fable 5 and Mythos 5 are the same model. Mythos goes to 200 approved partners. Fable goes to everyone else, with hidden capability limits on frontier ML work. The stated reason is safety. The result is that US labs build the best tools and then weaken them for the work that advances AI. DeepSeek V4 matches Opus 4.7 on agentic benchmarks and ships under MIT license with full weights. The question is not who builds the better model. It is who gets more people building with it. Some of the Stuff I took from SemiAnalysis, But this will go Nuclear way I don't know

When Fable 5 is used for frontier LLM development, it does not notify the user and instead limits the model’s capabilities through methods such as prompt modification, steering vectors, and PEFT. Anthropic estimated that this would affect approximately 0.03% of traffic.

TSMC alone now carries 14.2% weight in the MSCI EM index, more than all of India at 11.94%, Seven of the top 10 constituents are chip or AI companies. No Indian firm has been in that top 10 for the first time in 26 years. This tells you the index has become a semiconductor ETF with emerging market wrapping India doubled its GDP from $2.1 trillion to $4.3 trillion in the same decade the index says it underperformed. Measuring stick broke, not the economy Prakash calls India the biggest loser of the AI boom because of white collar service exports - Fair concern. But $700 billion in US hyperscaler capex this year sits in 5 companies, 2/3rd of S&P 500 earnings growth comes from 68 direct AI plays, each dollar of revenue making 32 cents pre tax profit. That is not a broad economy thriving. That is a narrow trade running very hot. India at 7.6% growth on a $4 trillion base deserves a different yardstick The most honest line in this column is that nobody can go against the AI trade because it is career risk. Fund managers are not making an economic judgment about India. They are making a self preservation decision. SpaceX is listing at $1.75 trillion. Anthropic filed at $965 billion. OpenAI at $852 billion. Three IPOs within months, combined value near $4 trillion, will vacuum allocator attention from every other market on earth. India averaged 6% growth through a pandemic decade, Still gets filed under zero interest.

Is it Possible to Break Culture? Must watch this podcast to understand what it means In my view, when you cannot change the operating system, it is only possible if users update themselves over time.

He went too deep and explained it in layman's language, which honestly shouldn't be allowed. When I talked about the OS, I meant it is such a high-barrier system that even a strong regime cannot easily tweak or control it @amitkilhor youtube.com/watch?v=6FNRVY…

HK @HU_7019

3 Followers 107 Following

Saurabh Shahapurkar @Saurya_SS

22 Followers 1K Following

Tony Mar @Tonylake88

67 Followers 920 Following

Mithun Mohanty @MithunMoha96467

15 Followers 87 Following

[email protected]... @saisharan365

20 Followers 750 Following

maybe @mrman_maybe

360 Followers 7K Following

Sreedhar reddy @Sree_dhar06

321 Followers 2K Following Hands that Help are Holier than Lips that Pray!!! Sabka Saath Sabka Vikas!!!

Sundar @sundarsgin

0 Followers 114 Following

Ben N @luft2020

29 Followers 95 Following

Krishna Popuri @PopuriKrishh

2 Followers 229 Following

Rajkumar @rajs1982

35 Followers 88 Following

venky @venky981

77 Followers 530 Following

Samas @samas777

1K Followers 2K Following We all root for our version of the best imperfection | Geek | Often West of the mighty Ganga, East of the mighty Mississippi

Lilavati- @baleLilavati

406 Followers 1K Following

Raman Sharma @ramanhimachali

709 Followers 6K Following Working with/on Turbo-Machinery for Oil & Gas sector. Passions: Being a dad, History , Reading , Arsenal.

slickman @slickman

0 Followers 2K Following

Narasimha @Narasimha0121

28 Followers 260 Following

Investever2 @investever2

14 Followers 373 Following

Pigeon @TailedPigeon

30 Followers 67 Following Lets Progress #UnitedWeStand - The Lone wolf dies. But the pack survives

Anirudh Agrawal, Ph.D... @Anirudh_Agrawal

2K Followers 5K Following Professor @bmluniv VisitSc @VSEPrague Ph.D. @CBSCph @HECParis @Veolia @Worldbank @FlameUniversity @JindalGlobalUni INSAL (twts and retwts are personal views)

Krishna @anumulakrishnaa

23 Followers 809 Following

Aman @25tanwar26

0 Followers 9 Following

Biswarup Burman @biswarup_burman

104 Followers 5K Following

sumit gupta @gsumit334

13 Followers 45 Following

Nagesh Kumar, PhD @nageshkum

2K Followers 1K Following Trade & Dev Economist; Director @ISID_India; Member, RBI’s MPC; ex-Director @unescap; @sswa_unescap; ex-DG @RIS_NewDelhi; @UNUWIDER; @GDP_Center; My views

Meet Jagani @jaganimeet89

25 Followers 389 Following E-Commerce (Profession) | Equity & Derivatives Trader (Passion) | For market insights, follow 👉🏻@marketmohmaya

Niket Kalra @moneyfornuffin

91 Followers 1K Following

Swaraj Bhad @SwarajBhad

53 Followers 1K Following

Nikhil D Argade @nikhil448

117 Followers 655 Following Passionate about investing, navigating the stock markets, and dissecting the latest blockbusters. 📈🎬

Samaresh Nandi @SamareshN2310

3 Followers 122 Following

nanami_7 @nanami_7714

0 Followers 4 Following

Pushkar Dhavale @pushkardhavale

109 Followers 524 Following Director: Pickle-Jar Investments Private Limited

Mohit Patil @PatilMohit76271

0 Followers 4 Following

Nick Grothe @NPGrothe

513 Followers 508 Following I built a team of 12 AI agents to do what analysts do. No employees. No fund (yet). Just the system, the data, and the thesis. Follow to see how far it goes

winnerx @twiter_winner

0 Followers 221 Following

Manish Tiwari @Manisht24947377

6 Followers 55 Following

Vibhor Agarwal @vibs98

136 Followers 308 Following Plastic Packaging (FMCG, Pharma, Cosmetic), Auto Parts, Drone Parts manufacturer | Injection Molding | 2+ decades experience. DM to work with us.📍India 🇮🇳

The Transcript @TheTranscript_

100K Followers 2K Following We write a weekly newsletter of quality quotes from Earnings Calls | Editor: @Skrisiloff | Lead Author: @ekmokaya | Publisher: @Avondaleam |

Sambhav Capital, CFA @sambhavcapital

371 Followers 263 Following CFA. Simple rules. High conviction. Long runway. Managing family portfolios with discipline and calm.

SemiAnalysis @SemiAnalysis_

103K Followers 27 Following

The Claude Portfolio @theaiportfolios

242K Followers 15 Following *Not affiliated with Anthropic. A public project to see which LLM outperforms the market. $150M invested alongside Grok, Chat, & Claude on @joinautopilot

Joe Weisenthal @TheStalwart

443K Followers 7K Following One half of Bloomberg's Odd Lots Podcast. One quarter of Light Sweet Crude.

hunter @hxxntrr

37K Followers 670 Following I secure 0% interest capital for business owners, and repair credit. Work with me here 👉https://t.co/XjgkMFjiem

Gavin Baker @GavinSBaker

250K Followers 6K Following Managing Partner & CIO, @atreidesmgmt. Husband, @l3eckyy. No investment advice, views my own. https://t.co/pFe9KmNu9U

The Kobeissi Letter @KobeissiLetter

2.0M Followers 629 Following Official X account for The Kobeissi Letter, an industry leading commentary on the global capital markets. Email us: [email protected]

Samit Vartak CFA @SamitVartak

61K Followers 54 Following Chief Investment Officer, SageOne Investment Managers LLP. Money shouldn't overshadow the bigger purpose of life.

Jeff Pu @sssjeffpu

29K Followers 46 Following Tech Enthusiast. 20 years tech equity research + industry.

Jukan @jukan05

143K Followers 319 Following Tech otakus save the world | Not Investment Advice | DYODD

The CapTable @thecaptableco

10K Followers 14 Following Actionable news. Smart analysis. Better decisions. Sign up for The CapTable, @YourStoryCo product.

Pranay Kotasthane @pranaykotas

15K Followers 293 Following Deputy Director @TakshashilaInst Tech Geopolitics | Cohost @puliyabaazi Co-writer: https://t.co/wU8xCe8Uu9 Co-author of 3 public policy books Views my own

Benjamin Todd @ben_j_todd

19K Followers 202 Following Founder @80000Hours Use your career to tackle the world's biggest problems 🦑 New book with Penguin: https://t.co/Tjs5Pig21B

Andrew Curran @AndrewCurran_

53K Followers 18K Following 🏰 - I write about AI, mostly. Expect some strange sights.

Marc Andreessen 🇺�... @pmarca

3.7M Followers 31K Following You’re not talking to someone who woke up a loser. That loser attitude, that loser premise makes no sense to me.

Value Seeker @ValueSeeker_

10K Followers 549 Following Finding bargains across commodities, stocks, currencies. Deeper analyses on my Substack: https://t.co/nglwl0f7XA No investment advice.

ᴋᴀᴍʟᴇsʜ sɪ... @kkstau

73K Followers 657 Following Occasional columnist and regular calumnist | Storyteller at Teen Taal #TTStaff | History-Religion-Politics | Hi-Ur-En | BR-JH-UP

Kevin S. Xu @kevinsxu

16K Followers 3K Following Long-only investing @ Interconnected Capital; Writing @interconnect_ed; ex. GitHub, Obama White House/Commerce Dept; no one's quant

Sandeep @SandeepUnnithan

38K Followers 1K Following Editor-in-chief @chakranewz / YT. Author : Black Tornado, 3 sieges of Mumbai26/11 https://t.co/nmiOL1rxea Operation X https://t.co/FCWgNacMXF

Aakanksha @aakancvedi

23K Followers 59 Following escaping the spontaneous consensus of the hive mind

John Mearsheimer @MearsheimerJ

59K Followers 44 Following John Joseph Mearsheimer is an American political scientist and international relations scholar, who belongs to the realist school of thought

Claude @claudeai

1.5M Followers 2 Following Claude is an AI assistant built by @anthropicai to be safe, accurate, and secure. Talk to Claude on https://t.co/ZhTwG8d1e5 or download the app.

Rupak @RupakChatto

12K Followers 4K Following Federalism, History, Economics, Aviation. Tweets personal, unrelated to organisations I am affiliated with.

Zorawar Daulet Singh @Z_DauletSingh

21K Followers 4K Following Author • Geopolitics and international relations • https://t.co/QEK2qXfQSg

Lt Gen H S Panag(R) @rwac48

149K Followers 5K Following Free Spirit!Articles/RT posted without comments are not endorsements or my views,but posted for general information!

Patarames @Pataramesh

102K Followers 279 Following Open source (-only) military technology analyst Iran/Russia/China/DPRK/Israel https://t.co/Q44fKzbdgm Support: Via YouTube-Channel membership

abhay jain @abhayjainp

6K Followers 28 Following Global thematic, analyst. Building https://t.co/98E9fYiYkG

Sahil Nandu @sahilnandu

4K Followers 3K Following Head of Middle East & India - 13D Research. Global Macro Investing. Coach. Philosophy. Psychology. Motorcycles. Golf. Antiques.

Luke Gromen @LukeGromen

492K Followers 2K Following Founder & President, Forest for the Trees (FFTT). Author of "The Mr. X Interviews, Volumes I & II.” I never solicit via DM's. RT not endorsements.

Pranjul Bhandari @pranjulb

9K Followers 349 Following Chief INDIA economist and ASEAN economist @ a bank | Mason Fellow @ Harvard Kennedy School | Sucker for the arts | Supporter of the underdog

Evan A. Feigenbaum @EvanFeigenbaum

54K Followers 8K Following Leading voice on Asia, experienced across government, think tanks and markets. Advisor to two Secretaries of State, a former Treasury Secretary and global CEOs.

Xponent Tribe @XponentTribe

2K Followers 1 Following SEBI-registered PMS Registration number: INP000008516 Nothing we post here is Investment Advice

Manu Rishi Guptha @manurishiguptha

22K Followers 2K Following Fund Manager,Blogger,Hotelier,Golfer,Stoic I believe that sarcasm is the 'Soul of Wit' - if incomprehensible, pls unfollow. MRG CAPITAL https://t.co/z329hng85d

Yash Nerurkar, CFA @NerurkarYash

944 Followers 488 Following Equity analyst @Ionicwealth | Ex PPFAS MF

Kimi Product @KimiProduct

18K Followers 5 Following Kimi's Official Product Account. Model updates are on @Kimi_Moonshot Sharing the latest updates, features, and use cases to help you master the Kimi ecosystem.

Oguz Erkan @oguzerkan

121K Followers 536 Following Investor | The founder & writer of the Capitalist-Letters newsletter read in +180 countries

Shane Legg @ShaneLegg

81K Followers 66 Following Chief AGI Scientist & Co-Founder, Google DeepMind Work website: https://t.co/E4SyeGVYXk Personal blog: https://t.co/LL9JNdNpW1

Ray Dalio @RayDalio

2.2M Followers 93 Following Official account of Ray Dalio, founder of Bridgewater Associates, author of #1 New York Times bestseller 'Principles,' professional mistake maker

Amit Jeswani @Amit_Jeswani1

71K Followers 301 Following Founder and CIO at https://t.co/e5ry28zUPv, CFA, CMT

TheGladiator @TheGladiatorHC

52K Followers 924 Following Founder @_phoenixglobal | CIO @_phoenixfund | All info is general in nature. I'm paid a fee by stocks mentioned by @_phoenixglobal ARN 001308566.

You might like