きゃぴたる @equitycapicapi

かぶ。LS+材料デイトレ Tokyo Joined June 2024-

Tweets19K

-

Followers1K

-

Following510

-

Likes18K

中国ハーモニック減速機「来福諧波」が香港上場へーー国内シェア21%超、ヒューマノイド需要追い風 36kr.jp/498027/

フジクラの仕草どこかで見たと思ったら株クラの平常運転だった 「爆損」「完全なる死」「退場」 からの「LH」「YTD+150%」

"If all goes well, TSMC is aiming to start mass production of the glass core substrate in 4Q28–1Q29, to match the cadence of Nvidia's AI chip iterations." 👀

Breaking down TSMC's glass core substrate slide On June 11, at JPCA Show 2026 in Japan, TSMC gave a roughly 40-slide presentation titled "Advanced Packaging Technology Essential to the Evolution of AI" (AIの進化に不可欠な先端パッケージング技術). One slide from the deck, titled

停止されているFebleについてかなり急展開ですが、韓国で開かれたAnthropicのイベントで関係者が「数日以内に(in the coming days)使えるようになると確信している」と発言していたようで、意外と早くFableが戻ってくる可能性。 トップのアモデイがG7でトランプや閣僚と直接話した結果かもしれない

政治家の方にも直接申し上げたが、成熟した国で数十億~数百億円の会社を支援するのもいい。だが、エルピーダ(元NEC日立メモリ、現マイクロン)の数千億円の手助けが出来なかったことによる現在の100兆円規模の価値喪失や、東芝メモリの一部を外資に出資支援してもらうハメになった事を反省し、今後似たような事例を作らないでほしい、日本人として エルピーダの件は擦り続けていい話かと思う。あまりにも失った国益のケタが大きすぎる

容積率2倍はあつい! 》 再開発エリアの容積率を本来の600%から約1350%まで緩和する。 》再開発エリアの容積率を本来の約600%から1230%まで緩和する。 nikkei.com/article/DGXZQO…

A dinner at Versailles just became the setting for a major diplomatic breakthrough. President Trump personally signed the Iran memorandum of understanding Wednesday while meeting with French President Emmanuel Macron, a White House official confirmed. The agreement, which Iranian President Masoud Pezeshkian also signed, is now in effect to end the war and cancels the formal signing ceremony that had been scheduled in Geneva.

スペースX、AI新興企業カーソルを正式買収-企業価値600億ドルと評価 bloomberg.com/jp/news/articl…

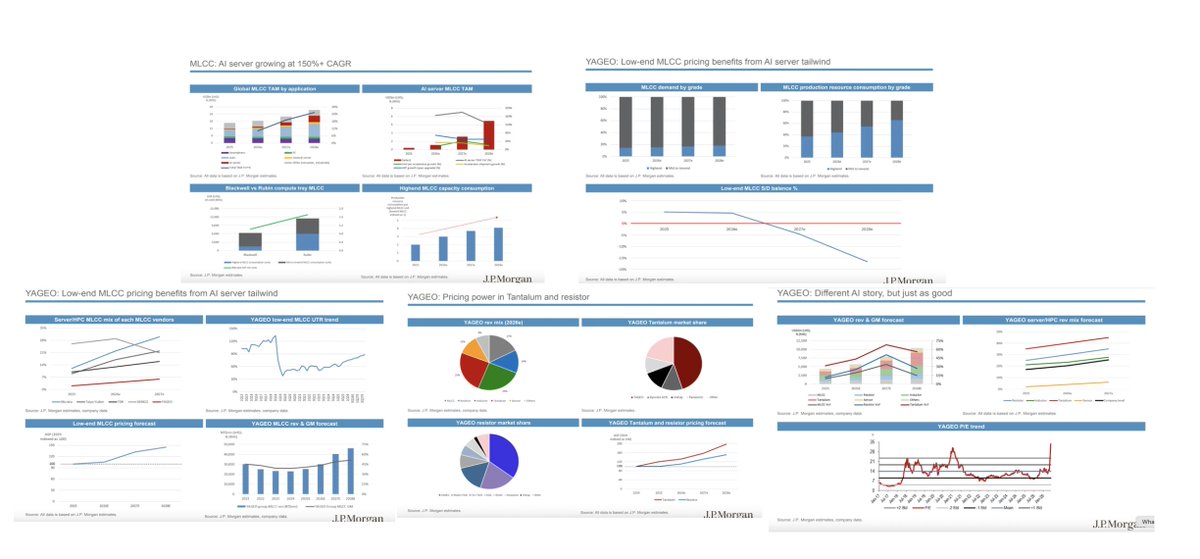

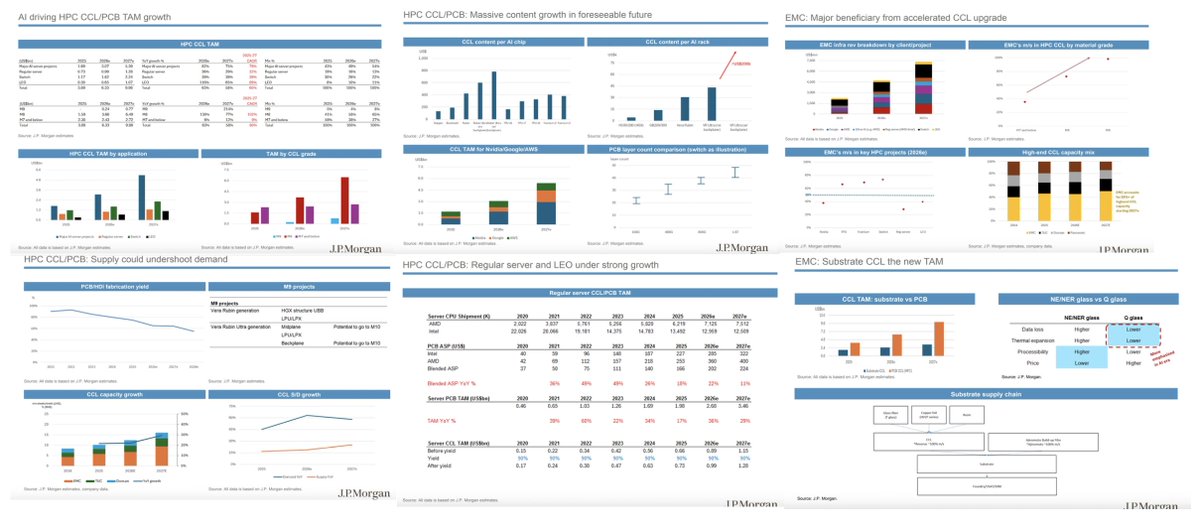

J.P.Morgan: Asia Passive Components, PCB/CCL, Substrate, and Testing Passive Components: > NVIDIA's upcoming Rubin platform will almost double the high-end MLCC consumption per compute tray compared to the Blackwell generation, alongside a higher blended ASP. > Production resource consumption per highend MLCC unit is expected to double between 2025 and 2028 compared to lowend MLCCs. > The supply/demand balance for low-end components is projected to plummet from a slight surplus in 2025 to a severe -15% to -20% shortage by 2028. > High-end units only make up a small fraction of total volume (growing slightly from around 15% to nearly 20% by 2028). However, the "production resource consumption" chart reveals that by 2028, making those complex high-end units will eat up over 65% of all manufacturing resources. > After bottoming out heavily around 2019 and staying sluggish for years, factory utilization for low-end parts for Yageo $2327.TW is coming back. It is climbing steadily back toward 90% through 2027 to meet the squeezed market demand. > ASP for low-end MLCC is projected to jump nearly 45% by 2028 compared to the 2025 baseline. > Yageo's MLCC revenue is projected to nearly double from 2025 levels to roughly NT$46 billion by 2028, pulling gross margins up toward a highly profitable 50%. > Yageo holds massive, top-tier market share slices in both Tantalum and Resistors. > Yageo's tantalum ASP will rise faster than resistors through 2028. > For Yageo, by 2027, server/HPC applications are expected to make up roughly 45% of tantalum revenue and 35% of resistor revenue, dragging the total company-level exposure up significantly. PCB/CCL: > HPC CCL market is expanding at a massive 60% two-year CAGR, ballooning from $3.89 billion in 2025 to $9.98 billion by 2027. > "Major AI server projects" are the undisputed locomotive here. They are growing at a 79% CAGR, jumping from $1.69 billion to $5.39 billion to command 54% of the entire market mix by 2027. > Legacy materials (M7 and below) are seeing their market share collapse from 59% down to just 27%. In their place, M8 grade is becoming the dominant mainstream specification, growing at a 102% CAGR to reach $6.49 billion. Meanwhile, next-gen M9 material enters the frame, exploding 214% YoY in 2027 to capture an 8% mix as advanced platforms ramp up. > CCL dollar value per chip steps up from ~$100 on Hopper to ~$200 on Blackwell, before surging to over $400 for Rubin. When moving to the Rubin Ultra generation with a full backplane configuration, the dollar content per chip skyrockets to nearly $800—an 8x increase from Hopper. Custom silicon is also driving this trend, with Google's $GOOGL TPU v7 and Amazon's $AMZN Trainium 2/3 hovering between $300 and $400 per chip. > An H100/H200 rack requires roughly $2,000 worth of CCL. The NVL-style GB200/300 architecture bumps that to ~$10,000. Vera Rubin hits ~$30,000, and a Vera Rubin Ultra rack with a backplane configuration absolutely explodes past $200,000 per rack—a massive 100x increase in dollar content compared to a standard legacy Hopper rack. > As networking speeds migrate from 100G up to 1.6T, the required PCB thickness and complexity scale dramatically, pushing average layer counts from ~20 layers all the way up to a 40-50 layer range for 1.6T architectures. > As boards become thicker and more complex (scaling up to 40–50 layers), manufacturing fabrication yields are collapsing. Yields have plummeted from a healthy ~90% in 2022 to an estimated ~65% in 2026, and are projected to dive below 60% by 2028. > NVIDIA's $NVDA Vera Rubin generation leverages M9 grade materials for its HGX structure UBB and LPU/LPX boards. The upcoming Vera Rubin Ultra generation pushes the limits even further for its midplane, LPU/LPX, and backplane architectures, introducing the potential to migrate entirely to M10 grade materials. > Key premium suppliers for CCL—Elite Material Co. $2383.TW, Taiwan Union Technology Corp. $6274.TW, and Doosan $000150.KS. > YoY demand growth is vastly outstripping supply growth. In 2026, demand growth peaked at over 60%, while supply growth crawled along at under 20%. This massive, widening gap confirms that supply could severely undershoot demand over the next two years. > Intel server CPU shipments are projected to continue shrinking from 22.0M in 2020 down to 12.5M by 2027e. Meanwhile, AMD $AMD shipments are steadily climbing from 2.0M to 7.5M over the same period. > Intel $INTC PCB ASP scales from $40 in 2020 to $322 by 2027e. AMD platforms command an even higher premium, with PCB ASP jumping from $42 to $400. This pushes the total Blended ASP up 11% to 22% YoY through 2027e. > Server PCB TAM is set to more than double from $1.69B in 2024 to $3.46B by 2027e (growing 36% in 2026e and 29% in 2027e). > Server CCL TAM (After Yield) mirrors this trajectory perfectly, compounding from $0.63B in 2024 to $1.28B by 2027e (assuming a steady 90% manufacturing yield baseline for these non-AI boards). > For EMC, total infra revenue is projected to climb from ~$2.3B in 2025 to over $4.7B in 2026e, and ultimately spike close to $7.5B by 2027e. The largest individual expansion drivers are NVIDIA, Google, and generic switching/networking architecture. > For standard M7 and below materials, EMC controls roughly 35% market share. That surges to ~73% for M8. By the time you reach ultra-low loss M9 materials, EMC commands a near-total monopoly with close to 100% market share. > EMC's estimated 2026 market share across specific tech stacks. 38% for NVIDIA, but skyrockets across major Big Tech custom silicon and networking plays: ~66% for Google TPU, ~70% for AWS Trainium, and ~74% for high-speed Switch trays. > While peers like TUC, Doosan, and Panasonic hold steady footprints, EMC's aggressive expansions mean it will single-handedly account for 50%+ of all global high-end CCL capacity starting in 2027e. > Substrate CCL is rapidly emerging as a major secondary growth vector. It is projected to climb steadily toward the $3.0B to $4.0B range by 2027e. Substrates: > By 2028e, the demand curve forces the theoretical utilization rate up toward a staggering ~135%. Because physical factories cannot run above 100% capacity, this gap represents an unprecedented structural shortage where demand vastly outstrips the world's physical manufacturing footprint. > In 2024, AI server & switch substrates made up just 26% of the global demand mix, while consumer applications dominated at 40%. By 2028e, that dynamic completely flips: AI server & switch will consume a staggering 75% of all global substrate demand, while consumer electronics wither away to just 11%. > AI Server & Switch Hyper-Growth is growing at a massive 67% CAGR from 2025 to 2028. Volume demand jumps from 2,448 bn nm in 2024 to an incredible 21,522 bn nm by 2028e. > Hopper sits at a baseline total size of 38,280 bn nm (12 layers). Blackwell steps up the complexity to 82,782 bn nm (14 layers). Rubin nearly doubles Blackwell at 144,918 bn nm (18 layers), while Rubin Ultra explodes to 322,040bn nm (20 layers). Feynman pushes boundaries even further, hitting 432,000bn nm with a staggering 24-layer substrate architecture. > Unimicron $3037.TW and Ibiden $4062.T maintain their dominant positions at the top of the stack. Unimicron's capacity scales from 73 in 2024 to 117 by 2028e, while Ibiden expands from 65 to 107 over the same timeframe. > Premium T-glass market is entirely cornered by the industry's two main titans. Unimicron captures the lion's share, securing 35-40% of total allocation, while Ibiden secures 30-35%. Everyone else is left to scramble over the remaining third. This secures Unimicron's raw material advantage during a time of extreme scarcity. > J.P. Morgan's margin projections for Unimicron from 4Q24 through 4Q27e, driven by structural under-supply, Unimicron's core Substrate margins are projected to climb from ~20% in late 2024 to above 50% by 4Q27e. This carries the blended company margin up to ~40%. > Chroma ATE $2360.TW overall semi/photon segment revenue jumps from around 10,000 NT$mn in 2025 to over 32,000 NT$mn by 2027E. The primary engines of this surge are SLT (System-Level Test) and Optical Comm testing, both expanding at a 100%+ CAGR. While optical comm YoY growth drops sharply after a 2026E peak, SLT YoY growth remains exceptionally strong, overtaking other legacy segments like Metrology and standard final test (FT). Read more here: kc9rsmb8u8.feishu.cn/file/UIQybxDfx…

This is an excellent report. I highly recommend reading it.

かぶかぶ @dijatc

56 Followers 71 Following

カブトムシ◆株... @Mkh68966652

259 Followers 274 Following 会社経営30代ママ👩🏻💼 子育て中👶億り人🙏 日本株450銘柄保有🇯🇵株主優待&高配当集めてます💓 読書📖+ヒットする漫画探しが大好き✨

ちょる子.日曜21... @tarekallam2011

88 Followers 1K Following 240万を元手に億り人になった豪運系投資家。二児のママ。PRのお仕事。【出演】NewsPicks、 ダイヤモンドZAI、日経マネー、日経CNBC、マネーのまなび、松井証券、田端大学レギュラー、楽待、トレアイ、みんかぶ連載/掲載記事

ケインズB @bg2006085

53 Followers 280 Following 今年から株式投資始めました。 主に個別株のスイングトレードをしています。 周りの方と成長していけたら良いなと思っています。 よろしくお願いします。

株ギャル😜🤘 ... @kabudekauitai

2K Followers 3K Following 地盤ネット信用全力で破産しちゃった😭 他にも借金あるので、1年は返済生活確定だね✨✨ もはや救いのないクソギャルですよぉ ₹˝ャʓササミ✌️( ,,ơ ̫く,,)💅💝 生きる意味を失ったアタイをせめて応援してね (๑ơ ₃ ơ)✨

株のカービィ @English_up

4K Followers 6K Following 投資歴10年以上のファンダメンタル派😺 新NISAで、国内バリュー株、投資信託をメインに積立中📈⤴️✨ 米国債ゼロクーポン複数年保有 #高配当 #NISA #SP500 #米国債 #ブルバ #株クラ

R @ka5463302146673

48 Followers 61 Following

suzuharu38 @suzuharu378

19 Followers 196 Following

飯田シート @StrangerThanPa8

260 Followers 791 Following 現役: 丸山、田中はると、石川、山田哲人、奥川、長岡 ⚾️歴代: 飯田、古田、土橋、稲葉、飯原、伊藤智、館山、五十嵐、石井弘、山本樹、川端 ⚾古田監督、宮本監督を実現したい。池山新監督に期待!!

_ @f0nbxAe6kb45538

54 Followers 273 Following

エバーフレッシ... @yarukizero54321

95 Followers 586 Following 関西在住🐙2023.10よりゆりゆると エルメスパトロール🍊してます!ヴァンクリもスッキ🍀#エルパト #オレンジパトロール

シーサー@兼業�... @stock_shisa

265 Followers 568 Following スキマ時間に日本株のトレードで稼ぐ会社員🏢 / ポイ活で貯めた100万円を元手にデイトレ/ 失敗トレードの反省記録も公開中📝 / 投資初心者の方、一緒に学びながら資産を増やしましょう! / #株初心者 #デイトレード #投資家さんと繋がりたい

かずきん@筋肉�... @kazukin_fitness

4K Followers 7K Following ダラダラ筋トレ歴15年のITエンジニア&投資家です🙌酒を飲みつつ3ヶ月で理想の身体になりました😭(上写真)YouTubeではゴリマッチョが多いですが「そこまでの筋肉目指してないんだけど…😅」という、ゆるトレニーなので、細マッチョ&主に30代以上向けの情報を発信🙌

パンナちゃん。 @panna_chan_dayo

297 Followers 2K Following

カブチャレ@日�... @kabu_challe

2K Followers 7K Following #日本株投資家 さんのための統計解析・スクリーニング・バックテストが細かく出来るシステムトレードサービスの中の人です。 初心者向けのトレードや投資情報を発信してます。 #個別株投資家 さん達の必須ツールを目指します✨ みなみなさま、ぜひ使ってみてください🥹 不具合や改善して欲しい点もどんどん教えてください〜!

ちょる子🐣日�... @kabu_st0ck

114K Followers 2K Following 240万を元手に億り人になった豪運系投資家。二児のママ。PRのお仕事。【出演】NewsPicks、ダイヤモンドZAI、日経マネー、日経CNBC、マネーのまなび、松井証券、田端大学レギュラー、楽待、トレアイ、みんかぶ連載/掲載記事⇒https://t.co/AfyI3k7uTE

メイディ(株) @meidy_macd

4K Followers 516 Following 29歳会社員一児パパ(23/03開始)|現在相場4年目突入|個別で稼いでNISA SP500満額埋め目指す|決算モメンタム投資法研究中|ブログやってます|23年-41.1%|24年+49.3%|25年-9.8%

Masa🌸 @conradosmendes

98 Followers 974 Following 外資系投資銀行でマーケット部門の役員を務めた後、運用会社を設立。再生可能エネルギー施設や不動産などの実物資産投資をコアとして安定リターンを得る一方、金融商品でトータルリターン向上を図っています。金融市場の大きな流れを的確に捉えられるように情報収集しています。

おぱ子@レバETF�... @sekata_404

853 Followers 2K Following レバナス/3倍ETFに夢を託す投資ベタ デイトレ爆損!退場寸前!! FIREへの道が遠のきました。 トレードは冷静に! 好物★3倍ETF $SOXL $TECL ☆短期はデイ、スイング←すぐ溶かす ☆長期は積立NISA(NASDAQ100)、iDeCo(全世界) ☆旧ジュニアNISAは爆益成長中💰️

にゃんまるコイ... @nyandogu_

226 Followers 1K Following 俺たちの天才松田とにゃんまるコインを愛する土。 8億NYAN以上保有。にゃんまるガチホ村の管理者。! own 800million NYANMARUCoins#にゃんまるコイン #俺たちの天才松田 $NYAN

Scorpions Capital @Scorpion_Fund

268 Followers 7K Following Activist short selling focused on frauds and promotes. Presume all tweets reflect short positions and biased opinion. Verify independently. Not inv advice.

Wowoo Official @WowooHQ_

194 Followers 2K Following A SocialFi protocol where trust becomes currency. Powered by Goodwill, fueled by Memes.

片山幹健(Tomota... @tomotake94

7K Followers 4K Following CVCでキャピタリスト/自身の会社でスモールビジネス投資。資金調達、M&A、IPOやHRtechなどのテクノロジー関連のニュース投稿をしています。

0 @toritoritorich

28 Followers 710 Following

トロピ@株アカ @toropi122993

1K Followers 374 Following

ハイキング👟 @meguu6363

15 Followers 1K Following

きゅーぴー @Jh9WGo91FjESMJA

237 Followers 2K Following クソ嫁に3度不貞行為された挙句、子供を連れ去られました。相手側親も共犯。虚偽DV。あのクズ共、絶対許さないからな。

爆損のもぐもぐ... @mogumogudonute

310 Followers 595 Following 日本株のデイトレ/スイングはじめて1年🔰中古本とYouTubeでスタート📖資金は200万で挑戦中。あれこれ手法を試したり迷走中💫

人見∧( 'Θ' )∧ @toriman777

158 Followers 1K Following 2022年に200万で投資スタート(入金なし)。 いつも損してて株クラのすみっこぐらしです。 東証養分ボランティア慈善活動家。 相互じゃない鍵の方は外しちゃうことがあります、ごめんねチュンチュン∧( 'Θ' )∧

にんじん食べる... @ninjin_taberune

33 Followers 98 Following

ゆうき@理系投�... @NS6sR6OwmaqvcHB

289 Followers 610 Following 日本個別株(2023年5月〜)|ファンダメンタルズ分析|プログラミング|暗号資産||物理学

Jeff Pu @sssjeffpu

34K Followers 47 Following Tech Enthusiast. 20 years tech equity research + industry.

David Sacks @DavidSacks

1.6M Followers 4K Following Tech founder & investor @Craft_Ventures @theallinpod. Co-Chair, President’s Council of Advisers on Science & Technology.

Anthropic @AnthropicAI

1.4M Followers 2 Following We're an AI safety and research company that builds reliable, interpretable, and steerable AI systems. Talk to our AI assistant @claudeai on https://t.co/FhDI3KQh0n.

Herman Jin @ShanghaoJin

80K Followers 597 Following Ex-Goldman Sachs Asia FICC Exec & Co-founder of Zen Family Office. Now diving into crypto, exploring blockchain's potential

qinbafrank @qinbafrank

145K Followers 1K Following Investor in AI、Crypto、TMT,跟踪最前沿科技趋势、野生宏观政经观察、研究全球资本流动性、周期趋势投资。记录个人学习和思考,经常出错常态掉坑爬坑。Runner🏃

김두한 @gimduha77994334

10K Followers 1K Following 타락한 영광스러운 도박중독자. 카지노의 수도승. 반지하 거주. 매크로, 국제 정치, 주식, 암호화폐, 철학

Alphatica @alphaticaio

12K Followers 58 Following Former HFM | Trading & Investing | Rigorous Quantitative Research | Sophisticated Strategies | Institutional-grade for all Investors | Not Investment Advice

500drachmas @500drachmas

2K Followers 61 Following 神奈川県相模原市の橋本というところに住んでいます 現在、Xの無料ユーザーに対する投稿制限により、ポスト数を絞っています

Knockouttrader @knockouttrader

2K Followers 270 Following Just a little goblin looking for the golden pot sharing information, discussing opinions, trading US and EU shares & options. No recommendations #DYOR

UKI @blog_uki

35K Followers 516 Following 日本株・暗号通貨トレーダー。機械学習や統計的手法でマーケットを探求しています。 @i_love_profitと2人で資産運用中。

Vaelis @Vaelis_X

6K Followers 36 Following I research bottleneck stocks, hidden suppliers, and physical infrastructure constraints before they become consensus. Semis · packaging · optics · power · NFA

EMSOne @EMS_One

662 Followers 6 Following EMSOneはEMS/ODM業界を専門的に取り扱うWebサイトです。FoxconnやCompal、Asusなど業界トップ企業から中小企業に至る企業ニュースならびに携帯電話・PC・Displayなどの産業別市場動向をタイムリーにお届けします。

雑学をまとめる... @zatsugakuinu

29K Followers 260 Following YouTubeチャンネル『雑学をまとめる犬』の中の人。専門は化。 🐶奇妙なグッズ達→ https://t.co/Q1RBpoCUZ1 🐶ご連絡✉️はこちらまで→ [email protected]

根岸理央 @RioNegishi

3K Followers 692 Following 羇旅辺土の行脚を行う投資家。 証券史・金融史専攻(予定)社史や株券を収集中! 偶にメディア露出。講演会やイベント登壇は多め。投資は中3から 四季報読破は15冊(大1から) 国立銀行の本店跡地巡り、旧街道踏破を実施中! 連絡はDMにてお願いします

SemiVision 🇹🇼 �... @semivision_tw

12K Followers 2K Following Expertise in Semiconductor Industry │Silicon Photonics│AI Industry│Supply Chain│ASIC│Ecosystem

サステップ @susteps_jp

6K Followers 811 Following ▶ガバナンス・ESG/サステナビリティ系の情報垂れ流しアカ ▶元バイサイドの責任投資家的な何か、現在は独立。問合せはDMまで。質問箱 https://t.co/wQ4E6qlUZf

メイディ(株) @meidy_macd

4K Followers 516 Following 29歳会社員一児パパ(23/03開始)|現在相場4年目突入|個別で稼いでNISA SP500満額埋め目指す|決算モメンタム投資法研究中|ブログやってます|23年-41.1%|24年+49.3%|25年-9.8%

UTokyo Finance Commun... @utokyo_finance

267 Followers 2 Following 東京大学 学生金融コミュニティ。 本コミュニティは、学習・分析・アウトプットを通じて、学生の実績形成と金融業界との接点を同時に生み出すためのコミュニティです。 学生募集フォーム: https://t.co/FWfH5vIvn1 東大に限定せず意欲的な学生を全大学から募集しています。

会田誠 『茶の�... @makotoaida

101K Followers 149 Following 美術家。困ったくらいの愛国者。作品集『会田誠のスクラップブック』https://t.co/IFRGD1wYnC 『性と芸術』https://t.co/COrpUg7mel

Linda Raschke @LindaRaschke

134K Followers 127 Following Private Trader, lifelong student of markets, retired top performing hedge fund manager, featured in New Market Wizards

親子上場解消か... @tosakoi1

5K Followers 362 Following 売り時下手で親子上場解消やMBO、M&AなどTOB狙いと優待銘柄に分散投資。TOPIXに勝って、年初プラス成績が毎年の目標。投資は基本ポジトーク。60歳での引退組なので守りの運用。優待廃止ラッシュに怯えながら、キターを叫ぶことは続けたい。投資関連ネタ中心に、高知観光推奨、演劇お笑い鑑賞ネタも随時。冗談妄想願望多し

ネットのシール... @seal_ya_san

83K Followers 552 Following ボンドロ購入支援🛒オプチャ1万人超㊗️抽選 再入荷通知 シール情報まとめます//フォローして通知をON待機 //📣 シル活 ボンボンドロップシール ハイライトもチェック⚡️ボンドロ速報→@bondoro_alert 🔔シール速報→@soku_alert

Scorpion Capital @ScorpionFund

84K Followers 206 Following Activist short selling focused on frauds and promotes. Presume all tweets reflect short positions and biased opinion. Verify independently. Not inv advice.

みみりん@投資�... @beauty_oe

20K Followers 1K Following Architect & Electrical Engineer. 工学諸島🏝️の島民の株好きです。米国株、NBISに集中してポストしています。 テンバガー保有株 NBIS

Fincept Corp @finceptcorp

532 Followers 0 Following FinceptTerminal is a AI-Powered Financial Terminal for Investment Research and Trading.(🌟20K+ Stars on Github)

Codex Studio @Codestudiopjbk

10K Followers 10 Following Codexガチ勢3人で運営|実務レベルのCLI活用・自動化を毎日発信|大学院生・ポスドク対象の開発プログラム参加|賞金30万円獲得|現在は上場企業とAIエージェントを共同開発中|AI時代はコンテキスト/ナレッジ管理が9割|組織全体への「 Codex × Obsidian 」の導入は下のHPからご相談ください👇

shinshin @stkinvest_blog

3K Followers 630 Following システムトレーダー歴15年。大手電機メーカー現場管理職。 株式・仮想通貨で自動取引トレーダー。botter。ブログ↓ https://t.co/QwNQBkPTg8

片山幹健(Tomota... @tomotake94

7K Followers 4K Following CVCでキャピタリスト/自身の会社でスモールビジネス投資。資金調達、M&A、IPOやHRtechなどのテクノロジー関連のニュース投稿をしています。

abc Crypto Insights @abc_trillion

10K Followers 71 Following abc(東証コード:8783)|クリプトをディーリングする上場企業🚀今すぐ知りたい #仮想通貨 をリアルタイム分析📈定期的なラジオ企画で最新トピック&にゃんまるを深掘り😼 abcの最新IR情報・クリプト系ニュース&記事もお届け🔔仮想通貨の限定情報やご相談等はDiscordへ↓

Datachain @datachain_jp

2K Followers 25 Following 創業期からのブロックチェーン技術のR&Dを土台に、ステーブルコイン事業、トークン化預金関連事業、法人向けウォレット、クロスチェーン基盤、プライバシー基盤などを展開しています。 English: @datachain_en

渡辺創太 @スタ�... @SotaOnchain

75K Followers 910 Following CEO: @StartaleGroup (@StartaleGroupJP) 世界のオンチェーン化を進めています。 英語アカウント:@WatanabeSota ブログ:https://t.co/vbIhCQ4dwm

株式会社Pacific M... @PacificMeta_ja

3K Followers 182 Following ブロックチェーンとAIで新しい社会のスタンダードを創る。構想から実装まで、企業の事業変革を一気通貫で支援。41ヵ国以上・260超のプロジェクト実績。

watacchi(additional) @watacchikasou

31K Followers 815 Following M.D. Founder @kudasai_japan @0xmakase_jp Diving into Web3 株式会社Omakase #Aurory

Polymarket Japan @polymarketjapan

56K Followers 4K Following 世界最大の予測市場。政治、ニュース、暗号資産、文化、スポーツ、テクノロジーなどの予測。日本公式アカウント🇯🇵

Yui Torikata @yui_torikata

3K Followers 605 Following Former energy balances geek at the @iea and energy analyst at the @ief_dialogue behind @JODI_data, now with @KPLER in quest of greater energy data transparency.

大場紀章(エネ�... @nuribaon

35K Followers 4K Following Noriaki Oba ポスト石油戦略研究所 代表。エネルギー安全保障問題を中心に、ポスト石油時代の日本の戦略について考えています。JDSCエグゼクティブフェロー。 PHP総研客員研究員。会社アカ(活動報告等) @postoiljp お仕事依頼→ [email protected]

エル @Capitalnvest

205K Followers 998 Following 資産2桁億。TV局取材依頼、Yahoo!ニュース掲載歴有り。 日本で一番影響力ある暗号通貨投資家。ビットコインを10年間ガチホする古参。2016年CoinCheck経営陣と会い仮想通貨参入。2020年4-10月BTC買いと呟き続け10倍。2024年2月に2025年10月に天井くると予測し1年9ヶ月固定ポストにし続け的中

Ren @renstocks_

38K Followers 87 Following Investing into the AI buildout ⚡️ 500% YTD Head of AI | Product Manager 10+ years DD and full thesis in https://t.co/4NlE3Jd7E7 NFA

DeepTokyo @x_DeepTokyo

1K Followers 266 Following

Ayesha Ufaq @Ufaq_RM

21K Followers 11K Following Introvert/Digital Marketing/Nature Lover/PTI/DM for collabs and PR

墨汁うまい(Bokuj... @bokujyuumai

73K Followers 147 Following イーサリアム及び仮想通貨(暗号資産)のリサーチ解説を10年しています。経営者/トレーダー/リサーチャー 厳選情報を速報/解説 ・DMMサロン→(@bokujyu_salon) ・コラム→(@nadanews_com) ・セミナー→(@sunward_t ) ・公式一覧→https://t.co/gBXypPqzHj

Aave @aave

698K Followers 63 Following The most trusted financial network. Earn, borrow, save, and swap.

SOU⚡️投資ニュ... @SOU_BTC

152K Followers 464 Following 資産運用・投資に必要な重要ニュースを日本最速で配信。米国株・仮想通貨・ビットコイン・AI・地政学まで網羅し、毎日発信。フォロー&通知オンで、マーケットで今知るべき情報がすべて手に入ります。Amazonアソシエイト参加中。Business inquiries: DM ✉️Trends for United States

You might like