Quant Beckman @quantbeckman

Quantitative Researcher & Dev. | Financial Data Scientist | Machine Learning Engineer | Mathematical Research | Algorithmic Trading Systems quantbeckman.com Fresh takes on Quant Research Joined July 2019-

Tweets4K

-

Followers12K

-

Following0

-

Likes843

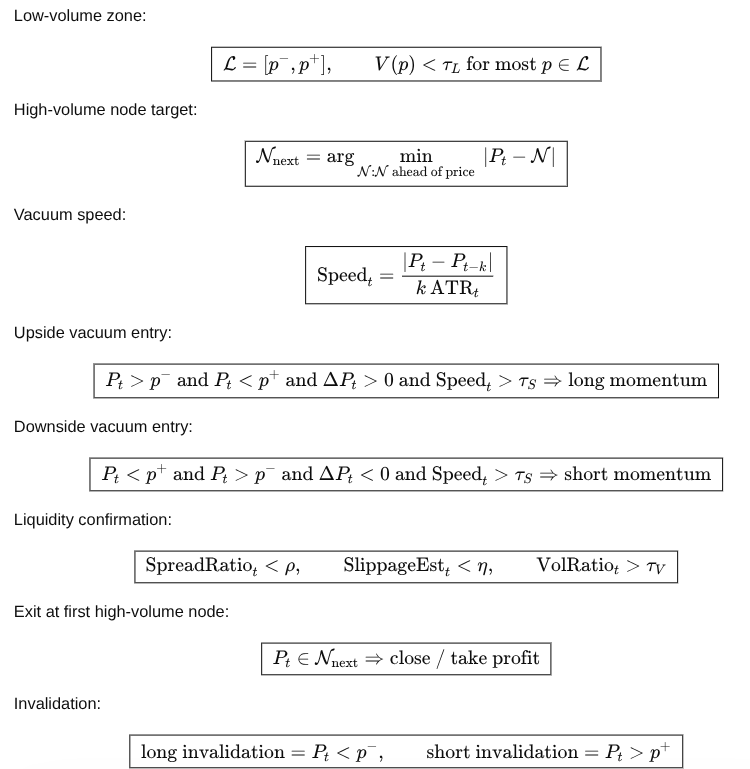

Some price zones contain little historical volume, so once price enters them, there is less resting interest to slow the move. This creates a liquidity vacuum where momentum can accelerate until price reaches the next high-volume node.

Selecting a feature == Selecting a market hypothesis

🟥For this one and more papers with code: quantbeckman.com

The inputs are normalized returns and MACD-style momentum features. That keeps the experiment clean, but it also means the paper is mostly testing whether attention over historical trend regimes improves trend-following, not whether the model discovers a broad transferable market structure.

@TerryBowl98 Not really. More variables? More noise (for the model)

One of the strongest biases a data scientist might bring to the industry is the belief that they need hundreds of features to predict something, when in reality they only need one (but a useful one). That's where research begins and nonsense ends.

The trading signal you research is never isolated. It is always linked to a specific context. The same signal can be valuable in one context and useless in another. Researching a signal means researching the conditions under which that signal expresses an edge.

These nodes often act as temporary balance areas because buyers and sellers previously agreed there. Trade the first clean escape from the node only when price leaves with acceptance, not just a wick.

Although the paper has several obvious flaws, including look-ahead bias, survivorship bias, and an excessively short out-of-sample period, it still provides an interesting comparison of portfolio construction methods such as MVP, HRP, and HERC. However, the key issue is the results themselves, they are mediocre.

🟥For this one and more papers with code: quantbeckman.com

The biggest pitfall is that the paper treats higher backtest returns as evidence of model improvement. It stacks several DQN extensions, tests them on a very small number of assets, and then reports large returns without enough controls to separate real edge from overfitting.

@TinnaHitesh It depends on what you want to model

And this is why your trading model will fail no matter what

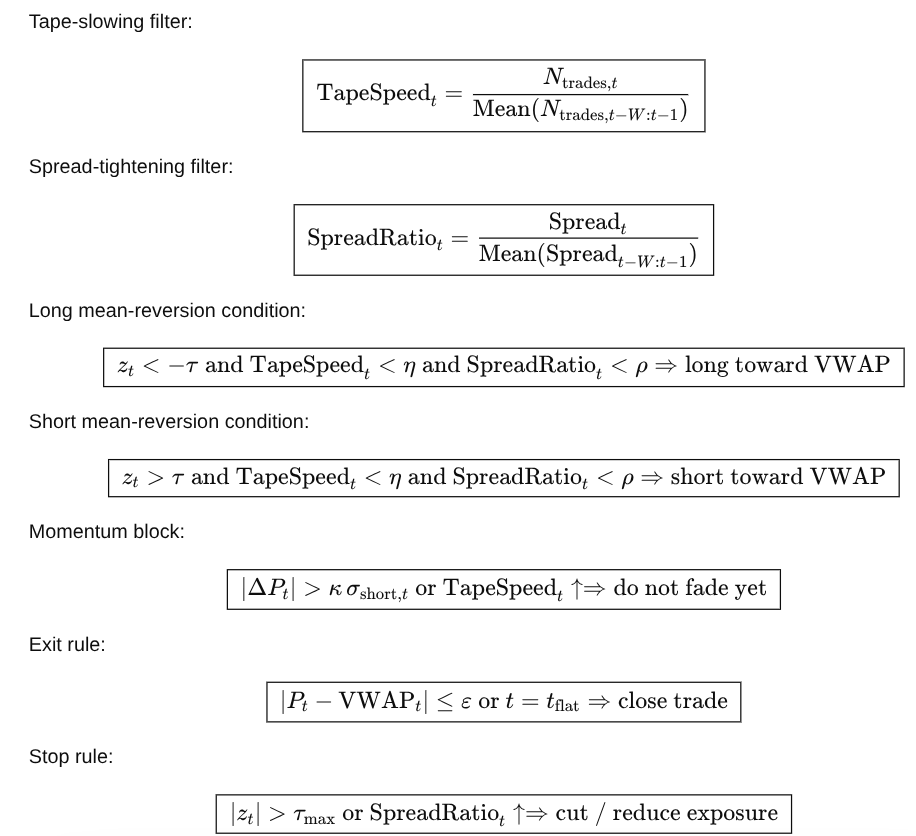

Large deviations from VWAP are faded only when the tape slows, spreads tighten, and immediate momentum weakens. This avoids shorting strength or buying weakness while the move is still being driven. The trade targets reversion back toward VWAP, not a full trend reversal.

🟥For this one and more papers with code: quantbeckman.com

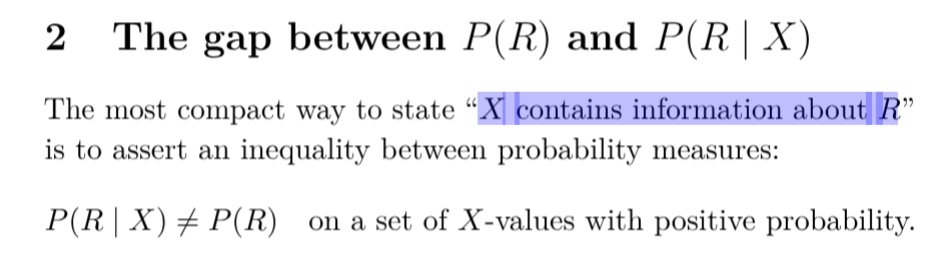

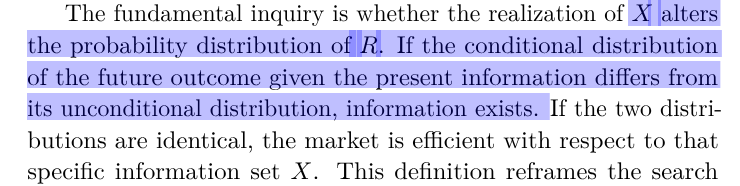

I like this definition of trading inefficiencies because it connects more directly to dependence relationships.

The authors admit that post-2004 EB predictions are less accurate because the 20-year rolling window fails to adapt to the market regime shift caused by information technology. EB could be interesting under a stable data-generating process, but markets are not stable

Ralph Sueppel @macro_synergy

18K Followers 410 Following Managing Director of Macrosynergy. Development of systematic macro trading strategies.

SpreadGreg @optiongreg

10K Followers 1K Following Gestor +11 años Derivados+Vola+Spreads+Padre de Familia. Tweets no recomendaciones https://t.co/gOU6keGwP4 https://t.co/7KmW0wTJv5

Gerard @Gsnchez

27K Followers 570 Following Programando en BQuant. Prof. MSc in Finance @bsm_upf, MEF @unav. 🎬 https://t.co/3IFs5Ae0Wq

X-Trader @XTraderdotnet

6K Followers 1K Following Portal y comunidad para traders. Todo sobre estrategias de trading y mercados financieros.

MKTSignals | Inversio... @mktsignals_org

3K Followers 310 Following Herramientas para tomar el control total de tus inversiones: #AmplitudDeMercado, #Amibroker, #Sistemas, #BaseDatos, Alertas de #MarketTiming y mucho más.

Artur Sepp: Systemati... @ArturSepp

10K Followers 337 Following All views systematic: https://t.co/hz2IJAhW7R & https://t.co/mGbPf9PtMf. Quant of the Year by Risk Magazine: https://t.co/7MeiDASJc2

SERSAN SISTEMAS @sersansistemas

5K Followers 678 Following 📊 25 años en trading 🤖 Sistemas en real (SYO+OYS) 📉 Sin método no hay consistencia 🎯 Empieza a automatizar ↓

QuantpTrader | Robust... @QuantpT

3K Followers 280 Following Robust algo trading Edges for traders using AmiBroker & EasyLanguage. For serious traders focused on risk, robustness & realism.

Ivan Scherman, CMT, C... @IvanScherman

61K Followers 1K Following CIO at https://t.co/eTgt1vPj4z Winner of the 2023 World Cup Championship of Futures Trading. Awarded as Best Audited Trader 2023/24 by Rankia.

Alex Ríos @Alexrios22

1K Followers 3K Following Ing. Electricista (UC) - Campeón WBC 2026. DT de TV y Fifero. Vinotinto - Juventino - Magallanero - Seguidor de Federer, Del Piero, Ferrari. #SiSePuede #SciTech

Sergi de Sersan @SergiSersan

4K Followers 3K Following Trader pro +20 años con track record público. Opero cada día con sistemas reales. Ahora enseñando trading algorítmico para que ganes con datos, no con emoción.

Juan Romero 📊 Quan... @quantforall

2K Followers 230 Following Acciones, ETFs, Futuros. Amibroker. Diseño sistemas que sobreviven en real. Comparto lo que realmente funciona. 📧Newsletter 👉 https://t.co/rKSc4dj1m8

Hobbiecode @hobbiecode

725 Followers 134 Following 📈Trader Algorítmico. Emprendedor. Make your life easier.

Rubén Martínez @rubenmesteban

8K Followers 498 Following Trader Algorítmico. Top 5 Campeonato del Mundo 2025.

Quantocracy @Quantocracy

24K Followers 197 Following Curated links from the quantitative trading blogosphere.

José Suárez-Lledó @SuarezlledoJ

4K Followers 703 Following Fondo Global Gradient | Bissan Wealth M | Moody's Analytics, PhD UPenn | Teaching @ Pompeu, IESE, ESADE. Finanzas, Economía, Aprendizaje, Problem Solving

vurimallanavaneeth @xnavaneethx_

0 Followers 31 Following

Suarezz @Suarez07192212

99 Followers 2K Following SZ Sports Analyst / Crypto Currency & Entrepreneur

•Mido’ Amr• @mido_Amr3

36 Followers 83 Following

Aakash Verma @0xAakashVerma

138 Followers 1K Following ||Web3/Crypto🚀 & AI Enthusiast🤖|| Footballer⚽❤|| Tech Community⬇️🚀

Rambo @pumpmaximalist

73 Followers 2K Following This account is a toy, if you take its content seriously, you might be autistic

Anup Singh @m0ch33z

379 Followers 3K Following Agribusiness, Dairy, Global macro, Foreign Exchange, Commodity markets, CO2, Emissions, Intelligence

Vincent Tan @TanVintwc

11 Followers 157 Following

eddie3201 @EddieChinese

6 Followers 50 Following

El hombre del saco @Alonso65Enrique

129 Followers 2K Following De pequeño me asustaban con el hombre del saco si me portaba mal, ahora se que no existe

Xaviher @Xaviher1231533

120 Followers 1K Following

Juno @Juno_Trades

2K Followers 1K Following Cancer Scientist || Butterfly Furu || Not a #Quant || #Fibonacci #Harmonics #ES_F $SPY #TA #charts #priceaction #stocks | @tradersofwallst Moderator | N.F.A.

olaf @san_pei77277

88 Followers 722 Following

DipXHunter @DipXHunter

129 Followers 249 Following

Girar @Giragirador

20 Followers 380 Following

Henko @henko1_

190 Followers 37 Following Everything is about your ego. Intercambio futuros con otros algoritmos y algunos humanos.

Arya Yaripour @ItsAryaYp

3 Followers 37 Following Interested In Mathematics, Computer Science & Finance.

Mario @mar1o_19

0 Followers 84 Following

Ali @shab__ro

90 Followers 408 Following کارشناسی عمران، چند سال دستوپا زده در علوم انسانی، دانشجو ارشد روانشناسی بالینی

WFCN 👽🖖🏼 @WalteneFred

75 Followers 897 Following Network Engineer. Não fui eu que lhe ordenei? Seja forte e corajoso! Não se apavore, nem se desanime, pois o Senhor, o seu Deus, estará contigo. Js1:9

Arjun Kapoor @Arjun72h

0 Followers 19 Following

TP @slate541

27 Followers 189 Following

Bailyn @aIZ5X7qmcq5661

0 Followers 14 Following

Kevin Ozee @CoachOzee

4K Followers 2K Following Christ follower. Husband, father and educator. Proud Texas A&M Aggie. This is my personal account.

Badasssh @everything1S0K

37 Followers 175 Following

Stacy Brovitz 🦇�... @sabuckeye1

44 Followers 105 Following

Shubham Shukla @shubhamshuklax1

22 Followers 314 Following Indian markets | Trading & investing Learning, observing, sharing real market lessons. Risk first. Capital always.

Mehul Asher @mehul_asher

83 Followers 325 Following

KAI @KaiofKings

102 Followers 195 Following Starborne Research Trading, Tech, Business Machine Learning, Neural Networks and Sophisticated Trading AI

Miles corp @MilesTradings

25 Followers 814 Following Specializing in Mercedes-Benz body part new and Grade A, fairly used. Quality component to keep your Mercedes looking and performing at its best. DM for inquiry

Mr P @tradewithmrp

14K Followers 134 Following 10+ års erfarenhet. Delar insikter & analyser för att hjälpa dig att utvecklas som investerare. Bluesky: https://t.co/Xlt6VTwmCk

hudson kisitu @hudson204

31 Followers 300 Following

Himanshu Patil @himanshugpatil

1K Followers 810 Following Passionate about #Stockmarket & #TechnicalAnalysis. Aspiring Quant. Hiking, Skiing. BTech IIT Mumbai, MS Purdue. Founder, https://t.co/10XeNm1b3R

Magnus @RealBlindsquirl

182 Followers 6K Following

Raj @RajkumarGupta26

598 Followers 5K Following Social Activist || Nature Lover || Blood Donation || Trekker || Runner || Software Developer || Trading || Retweets & Likes are not endorsements ..🤗Be Happy...

Sahand Ardehali @HyperProphit

584 Followers 746 Following Navigating chaos with reason. Markets are my mirror.

#neoswing_wave @neoswing_wave

291 Followers 1K Following

龙君 @zhumijun

7 Followers 219 Following

Rocky @Chinni_Rockz

91 Followers 2K FollowingYou might like