Randy Steuart @randysteuart

(mostly) credit guy lookin for bps and peops credit.ewingmorris.com Toronto Joined September 2025-

Tweets56

-

Followers1K

-

Following1

-

Likes3

"Every mispricing in a market is a cognitive artifact. Somewhere, a population of brains is compressing information in a way that does not match the complexity of the underlying reality. The price is not "wrong" in some abstract sense. The price is an accurate reflection of how participants are currently processing information. The opportunity exists because that processing has structural limitations." From What You're Actually Trading by @o_wutang Great piece. Markets have different "Compression Regimes"

Commentary only. Not investment advice. Ewing Morris has no position in Caesars Entertainment.

$CZR's palace intrigue. Hasn't been a great time to be a Caesars Bondholder. OTOH, a great time to be a Permitted Holder. cc: @sindap

The Acquired Podcast's Nintendo story is yet another example that the internet is the most meritocratic Access Conduit that has ever existed on planet earth. You can ‘Nintendo’ your way to anybody. Like Zuck... and Dimon and Ek and Jensen. On stage. At Chase Center. Amazing. It turns out that a singular, striking post/pod/essay can be the magnet that attracts someone who will change what's possible. "It's about the magnitude of the way a small number of people feel about episodes..." Power law mentality. Cut from @AcquiredFM

I'll be in midtown May 11 and 12, if anyone wants to chat co-ops + advance notice bylaw outtakes, why "Fundamental Change" > "Change of Control Triggering Event", the return of the dreaded Defeasance Threatened Tender as well as trade absurdly underfollowed X accts. DM's open.

Help first and see what happens. @EricJorgenson did this @naval noticed then @balajis then @elonmusk How about that. "Every day is an audition." Give your greatness. Appreciate the books Eric. Cut from Smart Friends Pod (7/2024)

it’s 1982. US treasuries are yielding 13%. bonds are trading at a huge discount. you’re exxon. you have excess cash. you issued bonds in the good times. and now you want to buy your bonds back in the 60’s. but most investors account for the bonds at book value (cost). selling them to you would trigger a writedown and getting yelled at. so you’re stuck. “why couldn’t you just ‘make-whole’ these bonds” you ask? (the standard option of buying back a bond very early at a yield close to treasuries) because it’s 1982. make-wholes were born in the mid 90’s. “you can’t do that” exxon might give up on it. but then a guy at morgan guaranty trust comes up with a solution. defeasance. retiring the bonds by way of buying and setting aside enough US treasuries to cover the bonds. the nuclear option. exxon defeases its 515mm of bonds for 60 cents on the dollar in treasury bonds. then every company wants to know what this newfangled defeasance thing is. nothing new under the sun.

@johnarnold "Amend and Extend" (Pretend), final answer "we had to" ¯\_(ツ)_/¯

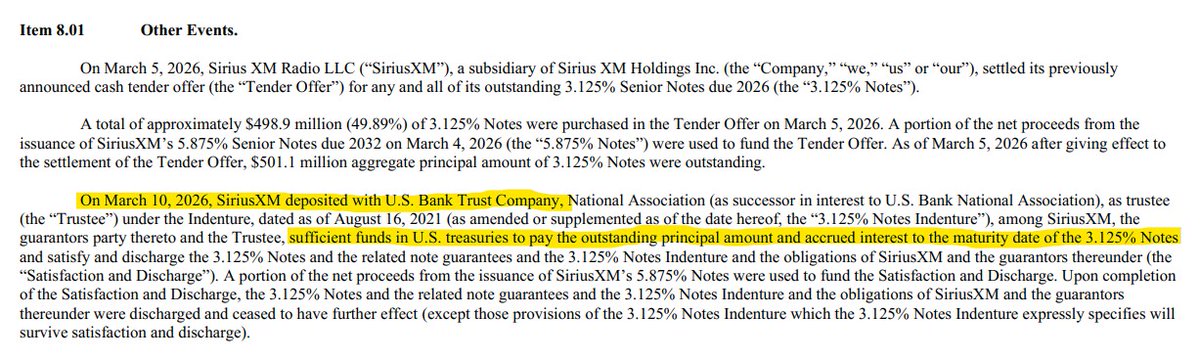

While the $EA Defeasance Threatened Tender (DTT) challenge plays out, $SIRI seen pulling a DTT on its 2026 bondholders to save a grand total of... ~50 cents. 50% declined to tender. Co confirmed the exercise of Defeasance to those dissenting bondholders. ...padme.jpg Not Investment Advice. Not Legal Advice.

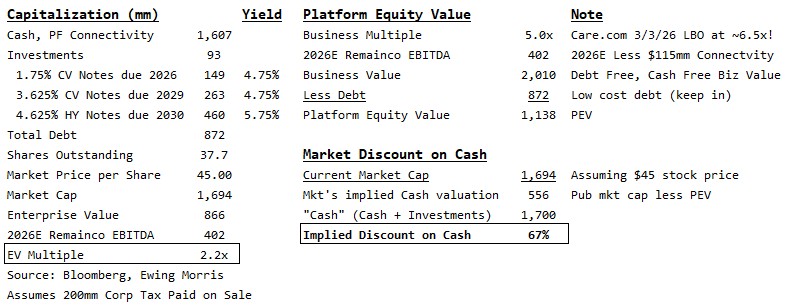

Busy morning in Digital Media. $ZD sells Connectivity for >10x. $1.2Bn cash. Stock is up >60%. Trades now at ***checks notes*** 2.2x PF EBITDA. Plus we've got a fresh transaction in a declining revenue "website" comp: Care.com. IAC sold it for ~6.5x EBITDA. Judging by the market reaction ($45), looks like the market is valuing Ziff Davis' cash and investments at ~30 CENTS on the dollar. Assumes remainco EBITDA is valued at 5x. Returning the cash to shareholders here seems like the most reasonable course of action. Interesting to compare $ZD's PF enterprise multiple of 2.2x to People.com debt (DOTMER) which trades low 9's yield at 4 times leverage. If the debt market is comfy going to 4x leverage on digital media assets, there are plenty of options here for Ziff and none of them have to do with buying other assets. Disclaimer: We own ZD at Ewing Morris. Views are our own, not investment advice. Sources: Bloomberg and Ewing Morris

The Roadmap Sell or Spin (a la Diller) Connectivity. Provides real-time data on internet and WiFi networks. News: IT’S NOT EVEN A PUBLISHING ASSET! It’s a subscription-based cash machine with excellent long term growth. With a ~45% EBITDA margin… 10x? 15x? Takes out the

If the credit market has ANY capitalistic sense left, this defeasance option should be wiped from new issues. The Optional Redemption covenant already affords issuers what they need to unilaterally retire their bonds.

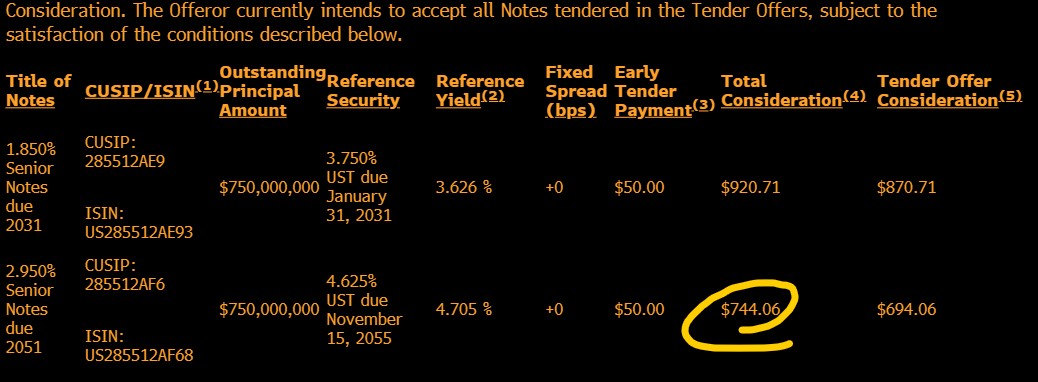

There it is. The most unwelcome development in public credit since LME: The Defeasance Threatened Tender. Today's casualty - the $EA 2051 senior bondholders. Traded just yesterday in the low 90's. This morning's tender... SEVENTIES. ...AND if BH's don't take the deal, the defeasance option is even worse... Kind of incredible this left tail risk wasn't more baked in. But then again, before this inaugural thread of mine calling it out in September, I had exactly zero followers. Public credit and shareholder engagement are my beats. Follow if interested. DM's open.

But the crazy thing is there's actually a big left tail now - EA could consider its option of defeasance. IYKYK. NIA, NLA, NAA (Not advice about anything).

William Karmin @WilliamKarmin

397 Followers 4K Following

Hedgehog @hedgehog3998

14 Followers 286 Following

BankingSlut @bankingslut

52K Followers 731 Following Yes I did that, and you would do it too for a check

BillsFanAnthony @BillsFanAnthony

75 Followers 399 Following Father of three strong to quite strong children (depending on the day). Toronto Finance guy. Buffalo Real Estate Guy. Food Guy. #BillsMafia.

crowdturtle 🐢 @crowdturtle

5K Followers 2K Following Investor in syndicated cash-flow-in-place real estate, public securities, loans, and #blockchain

Matt Reustle @ReustleMatt

6K Followers 1K Following "I'd like to solve the puzzle" Investments, Media, and Investment Media Former: Raven Capital, GS Research, Colossus/Business Breakdowns

Emanuel Dyankov @DyankovEma42828

6 Followers 134 Following

MW @mw_value

6 Followers 447 Following

alternativesyieldboi @alt_yield_boi

119 Followers 307 Following

Nico Milton @nico_milton_

161 Followers 3K Following posting about worthwhile things. not endorsement.

Squill @squill_capst

4 Followers 205 Following undergrad @NorthwesternU. interned in publics, PE, returning FT to PE. interested in anything macro & special sits related

Fortress Capital @DeepValue3

335 Followers 862 Following Private Investor. Debt markets. Derivatives. Tweets not advice.

Brendan Rafalski @Brafalski456

288 Followers 3K Following Public and private market investing; views are my own

MC @mehtache

67 Followers 2K Following

Good beagle boy @SP199393

185 Followers 4K Following L/S equities at hedge fund “The best time to plant a tree was 25 years ago. The second best time is now”

brad wood @brad_urbanmoose

22 Followers 471 Following

BAT @BATMongoose

3K Followers 2K Following Beat, raise, explore strategic options. All opinions sourced from much smarter ppl

Mark Hickey @Eagle2xx

18 Followers 365 Following

Rewardenn @Rewardenn

151 Followers 822 Following Value investing is the sole approach I have discovered that consistently increases one's wealth over the long term.

Craig U @craigersu

168 Followers 1K Following

Ypr @reversion2value

19 Followers 187 Following

H @TheEmperor1977

14 Followers 250 Following

CuppaJoe @cuppajoe80

48 Followers 94 Following

Jaeuk Sung @jsung0

42 Followers 180 Following

I Gotta Have More Pow... @IPowbell

36 Followers 286 Following

micromayven @micromayven

28 Followers 445 Following

totoroll @totoroll33

16 Followers 755 Following

Jay Siegel @JSiegel88

3K Followers 1K Following Fighting midwit tendencies daily On here for stories -- Corp DNA, the Deciders + their decision quality. Don't care what you think of Powell or Yellen .

Steve @Steve69446532

35 Followers 123 Following Small cap investor. Shameless borrower of great ideas. Occasionally insightful.

Thomas Yarbrough @tmyrbrgh

606 Followers 4K Following Love learning about the market and how I can help create the type of world I want to live in… Nashville TN

njefjay @njefjay

149 Followers 1K Following

Kiefer @kasel90

29 Followers 546 Following

Win @winoutcap

34 Followers 920 Following

PU @tokai_investor

50 Followers 237 Following

Friendly Capital Mana... @FriendlyCapMgmt

2K Followers 868 Following

dog100wbt @dog100wbt33081

25 Followers 246 Following

Redneck Capital @Camvas_ai

596 Followers 2K Following Equity L/S Analyst. Building a customizable Continuous Alpha Machine (dm for access)

Phenom Capital @phenomcapital

2K Followers 306 Following Engineer and investor. Looking for companies with inflecting earnings and a margin of safety. No investment advice.

DC @districtofcol

1 Followers 91 Following

Eric Chen @BornDwnUndr

322 Followers 1K Following

Nat Stewart @natstewart5

17K Followers 1K Following I write a concise small/micro cap focused newsletter for (mostly) professional investors. Deep value, GARP, special situations. Join my list below:

BLSH @buylowersellhih

89 Followers 932 Following

Basement Bullion @BasementBillion

96 Followers 239 Following

Edward O. Thorp @EdwardOThorp

22K Followers 2 Following Math professor, inventor, best-selling author, hedge-fund manager, gambler.You might like